June 18, 2019

Vignettes Improve Social Security Savvy

There’s an informal rule in journalism: put too many numbers in an article, and readers will drop like flies. A similar phenomenon might also be at work when someone looks at a Social Security statement filled with numbers.

There’s an informal rule in journalism: put too many numbers in an article, and readers will drop like flies. A similar phenomenon might also be at work when someone looks at a Social Security statement filled with numbers.

The statement, which is intended to help workers plan for retirement, shows the size of the monthly benefit check increasing incrementally as the claiming age increases. Yet many people still choose to claim their benefits soon after becoming eligible at 62, which means smaller Social Security checks, possibly for decades.

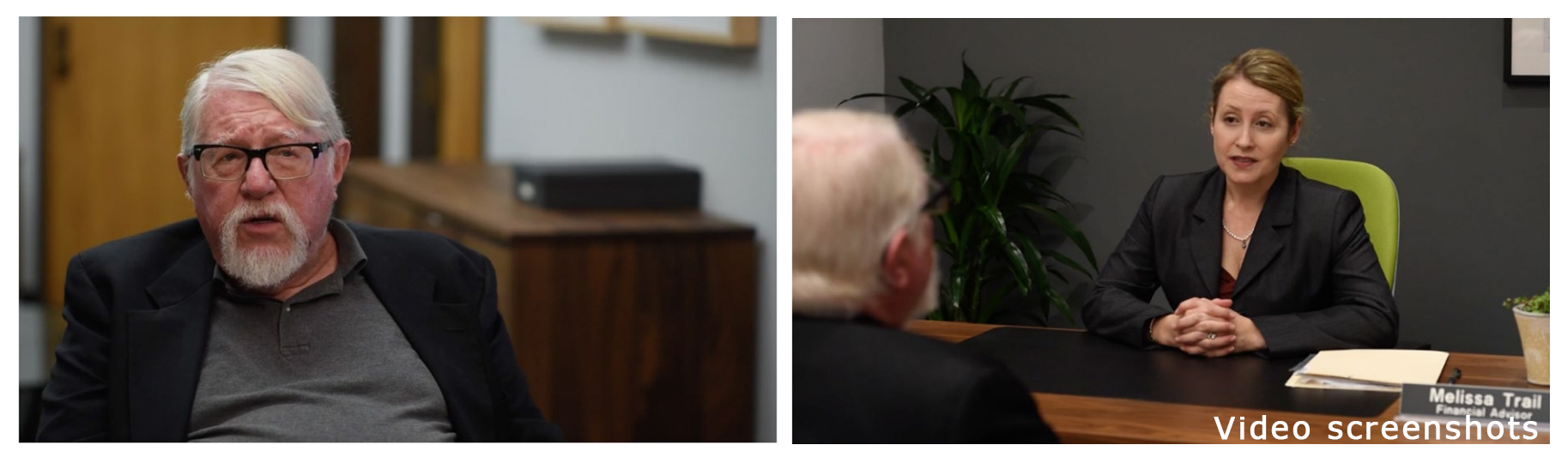

In a recent experiment, a friendlier approach proved effective in helping people process this information: tell a story. Researchers at the Center for Economic and Social Research at the University of Southern California created a fictional 3-minute video of a 62-year-old man talking with a financial adviser about retirement. The researchers showed it to workers between 50 and 60 years old.

Here’s one exchange in the video:

Adviser: [Social Security has] a tradeoff: you can decide to claim earlier. In that case, you would have a lower monthly benefit, but you’d get to enjoy these benefits for a longer period.

Worker: So if I claim sooner, I get less money per month? …Learn More

June 11, 2019

Self-employed Lose Some Social Security

Self-employed and gig workers who fail to report all of their earnings to the federal government will pay a price: a smaller monthly Social Security check when they retire.

Gauging the magnitude of this problem is tricky since the IRS doesn’t know how much is not being reported by a group of workers not easily identified in the available data. As a first step, new research derived estimates of the unpaid self-employment taxes that result from the under-reporting, using a combination of U.S. Census data on the workers’ incomes and past studies on the prevalence of the problem.

Specifically, the researchers found that more than 3 million self-employed people – construction contractors, small business owners, and other independent contractors – did not disclose some or all of their earnings to the IRS in 2014. This under-reporting translated to unpaid self-employment taxes of $3.9 billion to Social Security and another $900 million to Medicare.

An additional 2.3 million Americans sell goods and services on platforms like Airbnb, Lyft, and Etsy every month. A large share of these gig workers are not reporting all of their income either. Their under-reporting resulted in an estimated non-payment of $2 billion to Social Security and $500 million to Medicare in 2014.

In fact, the estimates are conservative, and the true level of the missing payroll taxes is probably larger, said the study’s authors, a tax expert at American University and a private policy consultant.

Independent contractors are most likely to be baby boomers over 55, while Generation Xers are more common on the online platforms. Self-employed people fail to disclose earnings for a couple of reasons: they are confused about the tax law or they want to increase their disposable income. But responsibility also falls on the platform companies that process payments for their workers and sellers, the researchers said, because the companies are not required to file 1099 earnings forms with the IRS for a majority of their workers.

Whatever the reasons for the underreporting, self-employed workers will one day get less from Social Security. This study raises an obvious question for future research: how much less? …Learn More

June 6, 2019

Class of 2019: Low Rent Key to Survival

The first and arguably most important decision a new graduate will make is how much to pay for rent.

If it’s too high, the rent – on top of those annoying student loans – will push out other priorities necessary to prevent financial trouble down the road.

Rick Epple, a certified financial planner in Minnesota’s Twin Cities area, counsels his daughter’s friends and clients’ children entering the labor force to keep their rent at around 20 percent of their income.

“Nobody ever talks about what they should spend,” he said. He worries about young adults who pay a third of their income – the standard recommendation – for an apartment. If the rent blows a hole in the budget, paying student loans every month and on time becomes a much bigger challenge.

A paycheck, Epple said, “just goes quick.”

A manageable rental payment also leaves room to prepare for the inevitable unexpected expense – and, yes, retirement. …Learn More

June 4, 2019

Husbands Ignore Future Widow’s Needs

The amount of money a widow receives from Social Security can mean the difference between comfort and hardship.

Husbands have a lot of control over how this will turn out. Each additional year they postpone collecting their own Social Security adds another 7.3 percent to the amount a future widow will receive every month from the program’s survivor benefit.

But husbands can be a stubborn lot.

Previous research has shown that a large minority fail to take their wives into account when deciding to start their Social Security. A new study confirms this in an online experiment designed to raise husbands’ awareness of the financial impact their claiming age could have on a spouse. The men’s ages ranged from 45 to 62.

In the experiment, the researchers displayed Social Security’s benefit information to the men three different ways. In the first format, a control group saw the basic information: the husband’s full retirement benefit, and then a link to a second page displaying his benefits for various claiming ages. A second format also displayed his full benefit, but the link went to a page with estimates of his widow’s survivor benefits, based on the husband’s various claiming ages – the later he files, the more she would receive. The third format had the same information as the second format, but it was presented on a single web page.

Regardless of the way the survivor benefits were displayed, the men weren’t persuaded to postpone their own benefits to one day help their widows. Potential explanations include their feelings about work, existing health issues, and whether they will get a defined benefit pension from an employer.

Whatever their motivation, simply educating husbands on the financial impact of choosing a claiming age “is unlikely to improve widows’ economic outcomes,” concluded the study by the Center for Retirement Research at Boston College.

The impact of widowhood is often significant. An average widow’s total income drops 35 percent when a husband passes away, the researchers estimated from financial data for married men who had retired. The earlier the husband had started his benefits, the larger the drop in the widow’s income after the couple’s second Social Security check stops coming in. …Learn More

May 28, 2019

Cars Separate U.S. Retirees from Germans

Florida

Retired Germans spend more days outdoors than retirees in this country. But when older Americans leave the house, they stay out longer.

What makes the difference? The car. Americans love their automobiles and overwhelmingly rely on them, according to a new study by MIT’s AgeLab. If they’re going grocery shopping, they might as well run their other errands.

Only about half of Germans, on the other hand, say driving is their favorite way to get around. And they venture out more frequently, because they can walk – or bike – to the market, which tends to be closer to home.

As people age and recognize the inevitability of their limitations, they begin to think more carefully about whether they will be able to remain in their homes. To gain insight into this issue, the AgeLab surveyed older Germans and Americans to compare their retirement experiences and satisfaction with their lifestyles – the AgeLab calls it “residential mastery.”

This goal is achievable for seniors everywhere, if they can find a way to continue to live healthily in a particular cultural and social environment. “Americans may reach residential mastery by having access to a car, ride-sharing or taxi services, while Germans may reach residential mastery by having shops and amenities in walking distance,” concluded an article in the Journal of Environmental Psychology.

In the survey, retirees in each country were asked what they need and what their neighborhoods provide. Both Germans and Americans put the most value on living close to healthcare facilities and their family and friends, who can provide the day-to-day support they need. They agreed on 12 of 17 aspects of their lifestyles – affordability, places to sit and rest, cultural institutions, green spaces, etc. – as being critical to them. …Learn More

May 21, 2019

Retirement Dates Don’t Always Fit Plan

Today, half of U.S. workers say they want to work past age 65 – in the 1990s, only 16 percent did.

Apparently, people are getting the message that, if they want to be comfortable in retirement, they will need to work as long as possible. However, good intentions don’t pan out for more a third of workers closing in on retirement age. And the older the age they had planned to retire, the more they fall short of the goal.

Researchers at the Center for Retirement Research, which sponsors this blog, wanted to uncover why people do not follow through. Their study was based on a survey that asked people in their late 50s when they planned to retire and then watched them over the next several years to see what they did and why.

Two factors – the researchers call them shocks – play important roles in pushing people to retire early. The big factor is health. One health-related reason is intuitive: when older people develop a new condition, they become more likely to retire earlier than they’d planned. A second reason is that, when setting a date, they over-estimate how long they’ll be able to work if they have already developed health conditions like arthritis, heart disease, or emphysema. …Learn More

May 9, 2019

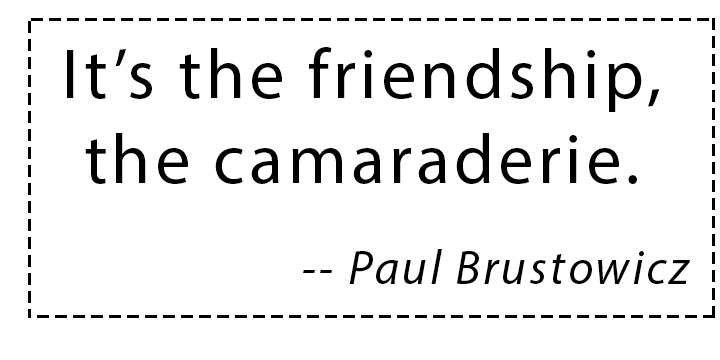

ROMEOs: Retired Old Men Eating Out

Every Thursday morning, five, six, seven of them meet for a hearty breakfast and freewheeling conversation at the Sunrise Bistro in Summerville, South Carolina.

The retirees’ talk careens from Tammany Hall and texting while driving to their military experiences and the aches and pains of old age. Several of the men had technical careers, so they recently dived deep into analyzing why a Coast Guard cutter carrying Zulu royalty crashed into a New Orleans dock.

“We talk about man things,” said Bob Orenstein, an 83-year-old Korean War veteran who is retired from a Wall Street computer firm. “Men are mainly loners frankly, but everybody has found something to identify with in the group.”

“We talk about man things,” said Bob Orenstein, an 83-year-old Korean War veteran who is retired from a Wall Street computer firm. “Men are mainly loners frankly, but everybody has found something to identify with in the group.”

The truth is that the ROMEOs – retired old men eating out – get much more than that from their weekly assemblies. “I think it’s just the friendship, the camaraderie,” said Paul Brustowicz, 74, a former jack-of-all-trades for an insurance company.

Friendship is the best antidote to isolation, which is dangerous for older Americans because it can lead to depression, poor health habits, and other problems. Most of the men in the breakfast club are South Carolina transplants, and their meetings have led to socializing and phone calls outside the group. Two of the men go deep-sea fishing together for redfish, and others share memories of growing up in New York or the tricks of the trade for constructing sailboat and railroad models. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.