April 16, 2020

Fewer Choosing Annuities in TIAA Plan

In a 401(k) world, purchasing an annuity is one way to turn retirement savings into a reliable source of income. But annuities have never been popular.

In a 401(k) world, purchasing an annuity is one way to turn retirement savings into a reliable source of income. But annuities have never been popular.

Now, a new study finds they are losing appeal even among some employees who historically purchased annuities at much higher rates than the general public: members of the TIAA retirement savings plan – one of the nation’s largest. Until 1989, TIAA required that retirees convert their savings into annuities.

Even in 2000, one out of two participants putting money in TIAA would eventually take their first withdrawal in the form of one of the annuity options the plan offers to retirees.

But by 2017, this number had dropped to about one in five, according to an NBER study for the Retirement and Disability Research Consortium that followed some 260,000 employees with careers at universities, hospitals, and school systems.

The researchers identified two distinct groups in terms of their annuity activity.

The first group tended to have smaller account balances and started tapping annuities in their retirement plans prior to the age when retirees are subject to the IRS’s required minimum distribution (RMD), which was, at the time of the study, 70½. Over the period studied, annuity selections by the first group fell from 57 percent to 47 percent.

The second group – people who had larger balances and didn’t touch their retirement accounts until after the RMD kicked in – saw their annuitization rate plummet from 37 percent to just 6 percent of the participants. …Learn More

April 14, 2020

More Cuts to 401k Matches are Coming

To conserve cash, some employers are suspending contributions to their workers’ 401(k)s. And if this downturn plays out like previous recessions, more will follow.

The handful of employers announcing suspensions in recent weeks include travel companies and retailers hit first and hardest by shrinking consumer demand, including Amtrak, Marriott Vacations Worldwide, the travel company Sabre, Macy’s, Bassett Furniture Industries, Haverty Furniture Companies, and La-Z-Boy.

Tenet Healthcare and a physician practice in Boston on the front lines of providing expensive coronavirus care have also suspended their matches. Employees, not surprisingly, are unhappy with these moves. An emergency room doctor told The Boston Globe that his organization’s decision comes as he is “working huge extra hours trying to scrape together [personal protective equipment] and otherwise brace for COVID-19.”

Employers are required to give their workers a 30-day notice and cannot stop the match prior to the 30-day period.

Suspending matching contributions has become somewhat of a recession tradition. In the months following the September 2008 market crash, more than 200 major companies rushed to do so, according to the Center for Retirement Research. The firms’ primary financial motivation was easing an immediate cash-flow constraint – not a concern about profits – the researchers found.

But cutting 401(k) contributions may be a small price to pay for mitigating layoffs, said Megan Gorman, a managing partner with Chequers Financial Management in San Francisco. “It might be a stop gap to help save the business in the long run,” she said. A typical employer matches 50 percent of employee contributions up to 6 percent of their salaries.

Amy Reynolds, a partner at Mercer Consulting, said the bigger danger for workers’ future retirement security is tapping their 401(k)s to pay their routine expenses in a tough economy. As part of the rescue package Congress passed in March, workers can withdraw up to $100,000 without paying the 10 percent penalty usually imposed on 401(k) withdrawals by people under 59½. “We want them to be thoughtful and consider other sources before they get to that,” Reynolds said. …Learn More

April 2, 2020

1st Quarter: Our Most Popular Blogs

People born smack in the middle of the baby boom wave, including many of this blog’s readers, are now in their mid-60s and have retired – or, at least, they were planning to retire before the stock market crashed.

Some of your favorite articles in the first quarter, based on the blog’s traffic, were about the nuts-and-bolts of retirement, including one that ranked retiree living standards by state.

The 10 most popular blogs listed below ran before the coronavirus changed our lives but they may still hold kernels of wisdom that will be useful in these trying times.

For example, one article reported on the $38 million in misplaced retirement funds from prior employers. If you think you have a long-lost retirement plan, search the unclaimed property account in the state where you worked.

Or, if you’d already committed to retiring before the market drop, it’s become more important to fashion a satisfying lifestyle. One blog explores how to prepare for retirement.

Our readers’ most popular blogs in the first quarter were:

Have You Misplaced a Retirement Plan?

Can’t Afford to Retire? Not all Your Fault

Mapping Out a Fulfilling Retirement

Most Older Americans Age in their Homes …Learn More

March 31, 2020

Boomers Facing Tough Financial Decisions

For baby boomers who thought they were on the path to retirement, the road is shifting beneath their feet.

Danielle Harrison, a financial planner in Columbia, Missouri, sees a raft of problems stemming from the COVID-19-induced economic slowdown.

Many older workers getting close to retirement age are taking big hits to nest eggs that were already too small. Some boomers who lacked pensions and were behind on saving tried in recent years to make up for lost time with a riskier portfolio in the rising stock market – now they’re experiencing the downside of that risk. Others are scrambling to pay expenses or maintain debt payments as their income drops, altering their financial security now and changing their calculations for the future.

“It’s really going to hurt people,” said Harris, who believes that some baby boomers who had planned to retire in the near-term may be rethinking those plans.

And she’s talking about the boomers who still have jobs. The layoffs have already begun and will continue. Economists estimate GDP will contract in the second quarter at an unprecedented 10 percent to 24 percent annual rate.

Evan Beach, a financial planner in Alexandria, Virginia, predicted that “People are going to get fired, and the people who get fired are not the 25-year-olds making $60,000. They’re going to be the 50- and 60-year-olds making $120,000.”

The economic stimulus package Congress passed last week could help, because it was designed to mitigate some job losses by extending loans to businesses that preserve their payrolls. It will do nothing to repair investment portfolios, however.

Beach and other financial advisers worry that panic decisions in this tumultuous time will only make things worse for boomers who, now more than ever, need to preserve their retirement resources.

Just as they did in the years after the 2008 financial market crash, some unemployed boomers will pound the pavement for a job and will scrape by – through odd jobs, short-term contracts, and unemployment benefits – rather than be forced into a premature retirement.

But Beach anticipates that many of them may have no other option than to claim their Social Security – the program’s earliest claiming age is 62. The problem with starting Social Security now is that it would permanently lock in a smaller monthly check. This goes against a central tenet of retirement planning, which is that many people would be better off delaying the date they sign up to increase a retirement benefit they will need for the rest of their lives.

Beach conceded, however, that claiming the smaller benefit now is not irrational for a couple with one laid-off spouse, only $2,000 in income, and $3,000 in expenses. If the laid-off spouse can start getting $1,000 from Social Security, he said, “that’s not irrational. That’s desperate.” …Learn More

March 12, 2020

Market Drops Hit Those Who Don’t Invest

Photo by T. Charles Erickson

How fitting that I would see the play “Sweat” on Feb. 28 – a Friday night at the end of a week in which the stock market dropped 12 percent and the specter of recession reared its ugly head.

The Pulitzer Prize-winning “Sweat” – I saw the Boston revival – is about the havoc the boom-bust economy and falling financial markets wreak on working people’s employment security and their personal lives. In fact, the timeline of the play is bracketed by 2000, when the stock market crashed, and 2008, when it crashed again.

At the beginning of each scene, a voice-over broadcasts the day’s bad financial news. The stock market never crosses the lips of the characters in the play, which is set in a local bar that is the social center of the working class town of Reading, Pennsylvania. Their chief concern is the fate of their jobs at the steel tubing plant. But the unspoken stock market is an invisible character shaping their plight.

Playwright Lynn Nottage got her inspiration for “Sweat” during visits to Reading over 2½ years. Two female characters and each of their sons work at the plant – very typical of a factory town. The bartender used to work there until he injured his leg. An immigrant who is a busboy at the bar briefly gets a shot at the American dream as a scab worker when the company locks the union out of the plant. There is tension between the immigrant and the long-time residents, and between the assembly line workers and the one worker who is promoted to management. But in the end, all of their lives are tragically upended by the plant closing.

Factories began shutting down in the 1980s, in part because U.S. manufacturers learned they could hire workers at much lower wages overseas. But manufacturing’s long-term decline was perpetuated by the 2001 recession, which was triggered by a market drop, and a second recession that began with the 2008 market collapse.

Which brings us to 2020. …Learn More

March 5, 2020

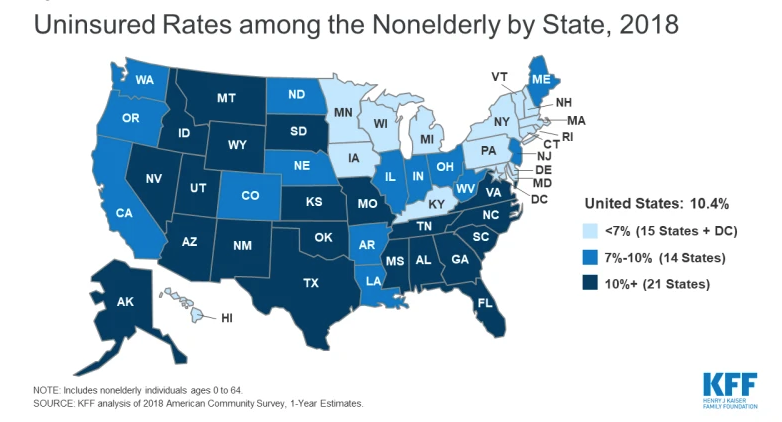

State Uninsured Rates All Over the Map

A decade after the passage of the Affordable Care Act, about one out of every five Texans under age 65 still do not have health insurance. Georgia, Oklahoma and Florida are close behind.

The contrast with Hawaii, Minnesota, Michigan, and New Hampshire is stark – only about one in 20 of their residents lacked insurance in 2018, the most recent year of available data, according to the Kaiser Family Foundation’s annual roundup of insurance coverage in the 50 states.

Despite this glaring disparity, the share of Americans lacking coverage has dropped dramatically across the board, including in Texas. Texas’ uninsured rate fell from 26 percent in 2010 to 18 percent in 2018. This translates to 2.3 million more people with health insurance. (Large populations of undocumented immigrants in states like Texas can push up the uninsured rate.)

States that had fairly broad coverage even prior to the Affordable Care Act’s (ACA) 2010 passage didn’t have as far to fall. For example, Connecticut’s uninsured rate is 6 percent, down from 10 percent in 2010.

One upshot of these two trends is that the disparity between the high- and low-coverage states has shrunk. Certainly, the strong job market gets credit for reducing the ranks of the uninsured. But millions of Americans who don’t have employer insurance have either purchased a policy on the insurance exchanges or gained coverage when their state expanded Medicaid to more low-income residents under the ACA.

For example, just two years after Louisiana’s 2016 Medicaid expansion, the uninsured rate had fallen from 12 percent to 9 percent.

But the initial benefits of the ACA seem to have played out. The U.S. uninsured rate increased slightly, from 10 percent to 10.4 percent between 2016 and 2018.

The share of people who are underinsured is also rising, the Commonwealth Fund found in a recent analysis. …

January 28, 2020

Education Could Shield Workers from AI

Not so long ago, computers were incapable of driving a car or translating a traveler’s question from English to Hindi.

Artificial intelligence changed all that.

Computers have advanced beyond the routine work they do so efficiently on assembly lines and in financial company back offices. Today, major advances in artificial intelligence, namely machine learning, have opened up a new pathway to expanding the tasks computers can do – and, potentially, the number of workers who may lose their jobs to progress over the next 20 years.

Machine learning works this way. A computer used to identify a cat by following explicit instructions telling it a cat has pointy ears, fur, and whiskers. Now, a computer can rapidly analyze and synthesize vast amounts of data to recognize a cat, based on millions of images labeled “cat” and “not-cat.” Eventually, the machine “learns” to see a cat.

But is this technological leap fundamentally different than past advances in terms of what it will mean for workers? And what about older workers, who arguably are more vulnerable to progress, because they have less time to see the payoff from updating their outmoded skills?

The answer, according to a third and final report in a series on technology’s impact on the labor market, is that advances in machine learning are likely to affect all workers – regardless of age – in the same way that computers have over the past 40 years.

And the dividing line, according to the Center for Retirement Research, will not be age. The dividing line will continue to be education: job options are expected to narrow for workers lacking a college degree or other specialized training, while jobs requiring these credentials will expand. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.