July 10, 2018

Meeting to Focus on Retirement Research

It’s not too late to sign up to attend the Retirement Research Consortium’s (RRC) 20th annual meeting in Washington on Thursday and Friday, August 2 and 3.

Its purpose is to provide RRC researchers from around the country an opportunity to present their working papers to colleagues, the press, policy experts, and financial professionals. The consortium’s studies are all funded by the U.S. Social Security Administration.

The researchers will cover a variety of financial and policy issues facing workers and retirees. Topics will include the gains in longevity when retirement is delayed, widows’ poverty, and an analysis of low-income workers’ earnings and retirement prospects.

Another paper explores the decline in the share of total U.S. earnings that are being covered by Social Security as increases at the top of the income scale outpace increases in the payroll tax cap. The links between money management and cognitive impairment among the elderly will be explored by one panel.

The members of the research consortium are the Center for Retirement Research at Boston College, which sponsors this blog; the University of Michigan Retirement Research Center; and the National Bureau of Economic Research.

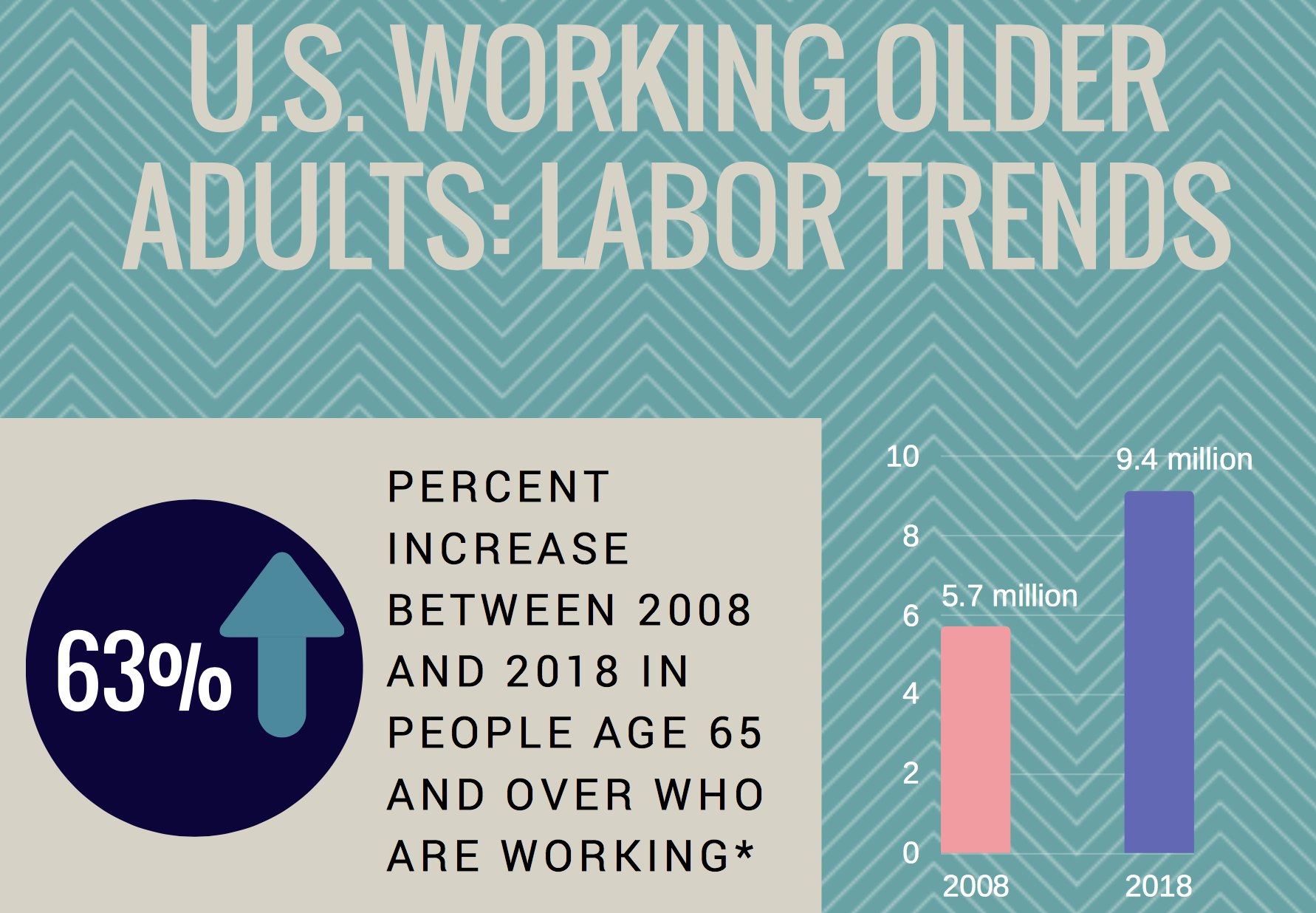

July 5, 2018

Boomer Bulge Still Impacts Labor Force

A theme runs through the infographic below: aging baby boomers are still a force of nature.

Created by Georgetown University’s Center for Retirement Initiatives, the infographic uses demographic data to show that boomers remain important to the labor market even as they grow older.

More than 9 million people over 65 work – a steep 65 percent increase in just a decade.

Two things primarily explain this increase. One reason is hardly surprising: the post-World War II baby boom that created the largest generation in history also created the largest living adult population (though Millennials will soon catch up).

On top of this, baby boomers are working longer for myriad reasons – among them, better health, inadequate retirement savings, and more education – which drives up their participation in the labor force.

To see boomers’ other impacts on work, click here for the entire infographic.

July 3, 2018

Readers Like a Travel Twist on Finances

Two of our readers’ favorite articles so far this year connected difficult bread and butter issues – personal finance and retirement – with a far more pleasant topic: travel.

The most popular blog profiled a Houston couple scouting locations for a dream retirement home in South America, which has a lower cost of living. Another well-read blog was about Liz Patterson, a young carpenter in Colorado who built a $7,000 tiny house on a flat-bed trailer to radically reduce her expenses – so she could travel more.

The downsizing efforts of 27-year-old Patterson inspired several older readers to post comments to the blog about their own downsizing. “From children’s cribs and toys in the attic, to collectible things from my parents’ 70-year marriage!” Elaine wrote. “Purging has been heart wrenching and frustrating and long overdue!”

The following articles attracted the most interest from our readers in the first six months of 2018. Topics ranged from 401(k)s, income taxes, and Americans’ uneven participation in the stock market to geriatric care managers. Each headline includes a link to the blog. …Learn More

June 28, 2018

Kids Figure into Retirement Plans

The grocery shopping for five is over, the family cell phone plan has been canceled, and the college tuition has been paid one last time.

So what’s next?

Newly minted empty nesters, having poured a couple hundred thousand dollars into raising each child, respond to their financial liberation in one of two ways. Some start saving more for their golden years. The others keep spending at that elevated level – but this time on themselves.

This personal decision, made at the critical juncture in the pre-retirement years, will have consequences for retirement – save more and things could turn out pretty well, or keep spending and jeopardize financial security in old age.

In the aggregate, at least some older households are taking the second approach. An analysis by the Center for Retirement Research at Boston College, finds that having children translates to “a moderate increase” in the risk that their standard of living will fall after they retire.

The researchers looked at the financial implications of kids from two angles. First, they used household data to estimate the sacrifices parents make – in the form of lower income – while they are raising children. Then they looked ahead to their retirement finances.

Compared with childless couples, parents in their 30s and 40s have about 3 percent less income for each additional child – some of this loss occurs when mothers work part-time temporarily or take time out for childbearing and childrearing. The income gap between parents and childless couples closes when parents reach their 50s and the kids start leaving the roost.

Less income over a lifetime translates to less wealth: parenthood reduces wealth by about 4 percent per child for workers ages 30-59.

The effects of children persist even after the transition from work to retirement. …Learn More

June 26, 2018

1 in 4 Can’t Afford a Summer Vacation

What a drag. One in four Americans said they can’t afford to take a vacation this summer.

The 3.8 percent unemployment rate is at its lowest since 2000, when the high-technology industry was going gangbusters. Despite the economy’s current strength, the cost of a vacation puts it out of reach for millions of people.

The average family of four spends about $4,000 on vacation, Bankrate said. Air fares don’t seem to be the issue – they are lower now than they were five years ago. But families living on a limited budget are more likely to drive, and the price of gasoline has shot up 25 percent over the past year, to around $2.90 per gallon.

Many people are shortchanging themselves on vacations, because they are “living paycheck to paycheck,” analyst Greg McBride said in a recent Bankrate blog.

Indeed, workers paid on an hourly basis can’t seem to get ahead. Their wage increases, adjusted for inflation, have been flat over the past year. Further, one in four U.S. households couldn’t come up with $2,000 even in an emergency, according to one widely cited study a few years ago. A summer vacation is probably out of the question for them.

Everyone needs a little time off to decompress and relax. Yes, it would be great to go on a deluxe fishing trip to Canada or cycle around Tuscany for two weeks, but there are more affordable ways to enjoy a few days off. A “staycation” is better than nothing. And the cost of a trip can be kept under $500 – one in four people do it, Bankrate said.

But cost isn’t the only reason people skip their vacation – family and work obligations also get in the way. A majority of workers, according to Bankrate, aren’t even using all of their paid vacation days.Learn More

June 21, 2018

Despite Medicare, Medical Expenses Bite

Medicare pays for the bulk of the medical care for Americans over 65, but a lot of their income is still eaten up by medical expenses.

The list of expenses is long. The lion’s share goes toward various insurance premiums – for Medicare Part B coverage, Part D prescription drug coverage, and supplemental insurance, whether Medigap, a Medicare Advantage plan, or employer health insurance for retirees. The remaining costs, for copayments and deductibles, are also significant.

These out-of-pocket costs, when added together, averaged about $4,300 annually per person, finds a new study by researchers Melissa McInerney, Matthew Rutledge, and Sara Ellen King of the Center for Retirement Research.

Out-of-pocket costs consume a third of the amount that retirees receive from Social Security, which is the most significant source of retirement income for a wide swath of the nation’s seniors, including many people in the middle-class. Half of seniors get at least half of all their income from the federal program.

The Medicare Part D prescription drug program has given some relief to retirees. After it became effective in 2006, the share of seniors’ income consumed by out-of-pocket costs declined slightly and then declined again after a follow-up reform of Part D began to close a big gap in drug coverage – known as the donut hole – in 2010. …Learn More

June 19, 2018

Work-Life Imbalances Spur Retirement

When young people are dissatisfied with a job or feel it intrudes too much on their personal lives, they find a new one. Not so easy for older workers.

Their decision is complicated partly because they have fewer employment options as they age, but also because they must ask themselves whether or not it’s time to retire.

A study out of the University of Michigan’s Retirement Research Center found that people in their 50s, 60s, and 70s often choose to retire when long hours, inflexible schedules, and work responsibilities don’t allow them to do what’s required to help a family member or a sick spouse or to enjoy more leisure time.

Many things are constantly pushing and pulling older workers toward retirement, from lower pay, job stress, or unrealistic job demands to accumulating their required pension credits or having enough money in the bank. But the focus here is on lifestyle.

Marco Angrisani and Erik Meijer at the University of Southern California and Maria Casanova at California State University used a survey of some 6,000 older workers that asks about work-life conflicts and then followed them for nearly a decade to see if such conflicts led to decisions to reduce their hours of work or retire altogether.

The main takeaway was that both older men and older women who’ve had a work-life conflict in the past two years are far more likely to retire. This may not be surprising for women, who are typically the default caregivers for an ailing spouse, parent, or even a grandchild. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.