January 14, 2020

Oddly, the Educated Pay Higher Fees

It’s smart to invest retirement savings in mutual funds that charge very low fees for one simple reason: the worker keeps more of his money and hands over less to Wall Street.

But in a study of people in their 50s and 60s who have retired or otherwise left federal employment, the people with the most education and the best scores on a standardized test were more likely to make what seems to be the wrong decision. Rather than keep their retirement funds in the government’s Thrift Savings Plan (TSP), which has extremely low fees, they transferred the money to much higher-fee IRAs operated by financial companies.

The $500 billion TSP – the world’s largest defined contribution retirement plan – is inexpensive in large part because it invests only in index mutual funds, which automatically track a variety of stock and bond market indexes and avoid the need to pay money managers to pick the investments. The annual fees for TSP’s index funds – known as expense ratios – are under 0.04 percent of the investor’s assets.

But over a 10-year period, about one fourth of the former federal employees rolled over the money saved during their careers into IRAs that typically had much higher expense ratios: 0.57 percent. On top of that, IRAs often charge additional fees for investment advice, pushing the potential total annual fees to well in excess of 1.5 percent. It’s possible that investing in an IRA could generate enough returns to make the extra fees worthwhile, but research has shown this is not the norm.

What explains the rollover decision? More educated people tend to have larger retirement account balances, raising the possibility that they were either seeking out financial advice or were targeted by advisors’ sales pitches. However, even among people with similar balances, those with more education were still more likely to roll over to IRAs.

It’s possible that they “perceive that they know what they’re doing” and want to take control of their investments “even when higher fees result,” the researchers said. …Learn More

January 9, 2020

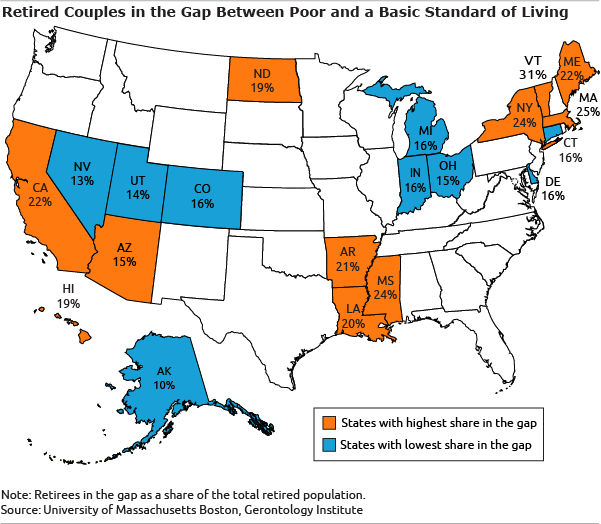

Retiree Living Standards, Ranked by State

How well you will live in retirement will depend on two things: your income and the local cost of living.

A new study that ranks each state based on how many of its retirees can meet a basic standard of living comes up with an interesting combination of places that are financially friendly – or not – to people over 65.

For example, who would expect Mississippi to be in the same company with California?

The cost of living in Mississippi is much lower than in California – and most states. But 31 percent of Mississippi’s retired single people and 24 percent of its retired couples fall into what the study calls the “gap” between being poor and having barely enough income to cover their basic expenses, according to a 50-state analysis by the University of Massachusetts’ Gerontology Institute in Boston.

A general way to think about the people inhabiting this gap is that, while they are above the poverty line, they are still financially insecure.

A general way to think about the people inhabiting this gap is that, while they are above the poverty line, they are still financially insecure.

“A lot of the folks who find themselves in the gap were middle class,” said Jan Mutchler, a U-Mass Boston professor and institute staff member. They have pensions or other income in addition to Social Security, she said, “and yet they’re still struggling.”

When the poor are added in, a total of 57 percent of Mississippi’s retired singles and 30 percent of its couples do not have the income required to pay for all of their essential household expenses, according to the analysis.

Like Mississippi, the share of older Californians who are feeling financially insecure is also one of the highest in the country: 34 percent of single people and 22 percent of couples. When poor retirees are included, the numbers rise to 54 percent and 27 percent, respectively.

Many people in California and Mississippi are having a difficult time – but for very different reasons. …Learn More

January 7, 2020

Credit Cards are the Most Stressful Debt

Debt is stressful. But did you know your stress level depends on the type of debt you have?

Credit cards cause far more stress than first mortgages and lines of credit, a study by Ohio State researchers finds. The more striking finding is that reverse mortgages, which allow people over age 62 to tap the equity in their homes, may reduce stress – at least temporarily.

The researchers used a simple example to illustrate the magnitude of credit card stress. Charging $640 on a card is as stress-producing as adding $10,000 to a mortgage. Credit cards are more stressful than home loans, because the balances on high-rate cards increase quickly when they’re not paid off, and the debt is not backed by an asset.

The researchers considered households to be debt-stressed if they said in a survey that they have had recent difficulty paying bills or have generally experienced financial strains.

This study focused on people over 62. As the share of older Americans carrying debt into retirement has increased, so have the amounts they owe. Debt arguably is very stressful for older workers, who have a dwindling number of years to get their finances under control before retiring, and for retirees, who have to live on fixed incomes.

The findings for reverse mortgages were nuanced – and interesting. Reverse mortgages create less stress than a standard mortgage and are much less stressful than consumer debt. On average, four years after taking out a reverse mortgage, the household’s stress level is 18 percent lower than it was at the time of the loan’s origination, according to the researchers, who did the study for the Retirement and Disability Research Consortium.

But things can change over time. Retirees often use federally insured reverse mortgages to pay off debt or as a regular source of income. But the amount owed on a reverse mortgage increases over time, because retirees do not have to make payments, and the interest compounds. (The loans are paid off when the owner either sells the house or dies.) …

Learn More

January 2, 2020

States Give Financial Help to Caregivers

On Jan. 1, Arizona residents caring for elderly or disabled family members became eligible for up to a $1,000 reimbursement from the state for expenses incurred in their caregiving responsibilities.

This is a trial program and the legislature allocated very little money – $1 million over two years – in a state with an estimated 800,000 residents caring for a disabled adult over 18.

But it’s a start.

Caregivers “aren’t asking for everything. They’re asking for a little bit to make their lives better,” said Elaine Ryan, vice president of government affairs for AARP, which has been on the forefront of advocating for such policies at the state level. “That’s the least we can do.”

Arizona’s program would defray a portion of caregivers’ spending. For older family members, this would cover technologies to aid older family members, such as hearing aids or computer programs, or shower grab bars and wheelchair ramps.

Like Arizona, state governments around the country, as laboratories for policy experimentation, have passed a hodgepodge of programs to support caregivers. Other bills approved in recent years range from New Jersey’s tax credit for military families caring for wounded veterans to Oregon’s paid family leave program for workers taking care of aging spouses, parents and grandparents.

The programs are a tacit acknowledgment of the enormous financial strain caregivers face – a strain that is only expected to grow and, increasingly, to affect Millennials as their baby boomer parents age.

However, it’s not easy to pass bills that require states to approve financial assistance or tax credits, because the work done quietly by family caregivers is often invisible and under-appreciated by the general public and federal and state legislators. …Learn More

December 31, 2019

Boomers Want to Make Retirement Work

The articles that our readers gravitated to over the course of this year provide a window into baby boomers’ biggest concerns about retirement.

Judging by the most popular blogs of 2019, they were very interested in the critical decision of when to claim Social Security and whether the money they have saved will be enough to last into old age.

Nearly half of U.S. workers in their 50s could potentially fall short of the income they’ll need to live comfortably in retirement. So people are also reading articles about whether to extend their careers and about other ways they might fill the financial gap.

Here is a list of 10 of our most popular blogs in 2019. Please take a look!

Half of Retirees Afraid to Use Savings

How Long Will Retirement Savings Last?

The Art of Persuasion and Social Security

Social Security: the ‘Break-even’ Debate

Books: Where the Elderly Find Happiness

Second Careers Late in Life Extend Work …Learn More

December 24, 2019

Happy Holidays!

Next Tuesday – New Year’s Eve – we’ll return with a list of some of our readers’ favorite blogs of 2019. Our regular featured articles will resume Thursday, Jan. 2.

Thank you for reading and posting comments on our retirement and personal finance blog. We hope you’ll continue to be involved in the new year. …

Learn More

December 19, 2019

NFL Rookie Took Finance Class to Heart

Joejuan Williams

Photo courtesy of the New England Patriots.

Joejuan Williams, a rookie defensive back for the New England Patriots, has received a lot of attention for his practice of saving 90 percent of his game-day paychecks. He credits his frugality to a personal finance class at his Nashville, Tenn., high school.

“It completely changed my life,” Williams told The Boston Globe recently. “I’m going to sacrifice now for me to be happy later.”

Williams, having signed a $6.6 million contract this season, isn’t exactly living on the edge. But keep in mind that these sky-high earnings are often temporary for football players. When one considers that the average NFL career lasts about three years, Williams is just playing it smart.

But read on in the Globe article, and a more complex and touching explanation for Williams’ frugality seems to emerge – one that revolves around a childhood watching his single mother live paycheck to paycheck.

“I’ve been stingy with money ever since I was young just because I saw what my mom had to go through,” he told the Globe. He said that he has paid off his mother’s student loans and purchased a car for her.

Although he credits the influence of his personal finance class, psychologists say that adult financial behavior has deep roots in childhood experiences like Williams’. In fact, endless research papers have debunked the effectiveness of financial education. There are numerous reasons for this, including a widespread aversion to math. Human nature is another obstacle: people regularly sacrifice their long-term goals to whim – credit card spending is the classic example.

Williams is different. He has his eye on the future. He is focused on one long-term goal for himself – investing his savings for the future – and one goal for his mother.

“I’m going to give my mom a home,’’ he said. “That’s the only big purchase I have my eyes on.’’

Williams’ high school finance class clearly influenced him. But maybe the lessons stuck because he took them to heart.

Squared Away’s regular posts will return Dec. 31. …

Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.