Posts Tagged "401k"

April 1, 2021

What the Research Can Tell us about Retiring

It’s difficult to envision what life will look like on the other side of the consequential decision to retire.

But research can help demystify what lies ahead – about the decision itself, the financial challenges, and even the taxes. Readers understand this, as evidenced by the most popular blog posts in the first three months of the year.

Here are the highlights:

The retirement decision. The article, “Retirement Ages Geared to Life Expectancy,” attracted the most reader traffic. Myriad considerations go into a decision to retire. But a sense of whether one might live a long time – because of good health or simply seeing that parents or neighbors are living unusually long – is a compelling reason to postpone retirement either to remain active or to build up one’s finances to fund a longer retirement.

A recent study found that as men’s life spans have increased, they have responded by remaining in the labor force longer, especially in areas of the country with strong job markets and more opportunity. This is also true, though to a lesser extent, for working women.

The planning. The second most popular blog was, “Big Picture Helps with Retirement Finances.” It described the success researchers have had with an online tool they designed, which shows older workers the impact on their retirement income of various decisions. When participants in the experiment selected when to start Social Security or how to withdraw 401(k) funds, the tool estimated their total retirement income. If they changed their minds, the income estimate would change.

The tool isn’t sold commercially. But it’s encouraging that researchers are looking for real-world solutions to the financial planning problem, since the insights from experiments like these often make their way into the online tools that are available to everyone.

The taxes. It’s common for a worker’s income to drop after retiring. So the good news shouldn’t be surprising in a study highlighted in a recent blog, “How Much Will Your Retirement Taxes Be?” Four out of five retired households pay little or no federal and state income taxes, the researchers found. But taxes are an important consideration for retirees who have saved substantial sums. …Learn More

April 14, 2020

More Cuts to 401k Matches are Coming

To conserve cash, some employers are suspending contributions to their workers’ 401(k)s. And if this downturn plays out like previous recessions, more will follow.

The handful of employers announcing suspensions in recent weeks include travel companies and retailers hit first and hardest by shrinking consumer demand, including Amtrak, Marriott Vacations Worldwide, the travel company Sabre, Macy’s, Bassett Furniture Industries, Haverty Furniture Companies, and La-Z-Boy.

Tenet Healthcare and a physician practice in Boston on the front lines of providing expensive coronavirus care have also suspended their matches. Employees, not surprisingly, are unhappy with these moves. An emergency room doctor told The Boston Globe that his organization’s decision comes as he is “working huge extra hours trying to scrape together [personal protective equipment] and otherwise brace for COVID-19.”

Employers are required to give their workers a 30-day notice and cannot stop the match prior to the 30-day period.

Suspending matching contributions has become somewhat of a recession tradition. In the months following the September 2008 market crash, more than 200 major companies rushed to do so, according to the Center for Retirement Research. The firms’ primary financial motivation was easing an immediate cash-flow constraint – not a concern about profits – the researchers found.

But cutting 401(k) contributions may be a small price to pay for mitigating layoffs, said Megan Gorman, a managing partner with Chequers Financial Management in San Francisco. “It might be a stop gap to help save the business in the long run,” she said. A typical employer matches 50 percent of employee contributions up to 6 percent of their salaries.

Amy Reynolds, a partner at Mercer Consulting, said the bigger danger for workers’ future retirement security is tapping their 401(k)s to pay their routine expenses in a tough economy. As part of the rescue package Congress passed in March, workers can withdraw up to $100,000 without paying the 10 percent penalty usually imposed on 401(k) withdrawals by people under 59½. “We want them to be thoughtful and consider other sources before they get to that,” Reynolds said. …Learn More

February 25, 2020

Have You Misplaced a Retirement Plan?

Wouldn’t it be nice to find some money sitting in a long-forgotten retirement account somewhere?

It’s not hard for workers to lose track of an old account as they move from employer to employer, often across state lines. Each state government keeps a repository of unclaimed property – most have been doing this since the 1980s – and residents and former residents can check online through a simple name search in the state’s unclaimed-accounts database.

But not everyone takes the trouble to search for the money or is even aware it exists. So billions of dollars have accumulated nationwide in various types of unclaimed accounts, including retirement plans, insurance policies, trusts, and brokerage and bank accounts – so much so that firms have sprung up that will do the legwork required for individuals to claim their money. But little has been known about how much sits idle in unclaimed retirement accounts.

A new study estimates conservatively that about $38 million, accumulated over many years in some 70,000 retirement savings plans nationwide, had not yet been claimed in the states’ property accounts as of 2016. Most of these are 401(k)-style plans but they also include IRAs and pension checks.

The average account value is only about $550. But the largest ones are anywhere from $5,000 to $13,000, which could be meaningful to retirees who are struggling financially. …Learn More

February 6, 2020

Can’t Afford to Retire? Not All Your Fault

Three out of four members of Generation X wish they could turn back the clock and get another shot at planning for retirement. One in three baby boomers say don’t think they’ll ever be able to retire.

“Overwhelmingly, Americans are stressed about their current – and future – financial situation,” the National Association of Personal Financial Advisors said about these new survey results.

Regrets about not planning and saving enough are enmeshed in our thinking about retirement. But it is really all your fault that you’re not getting it done?

The honest answer to that question is “no.” There are big gaps in the U.S. retirement system that make it very difficult for many to carry the responsibility it places on workers’ shoulders.

I predict some of our readers will send a comment into this blog saying, “I worked hard and planned and am comfortable about my retirement. Why can’t you?”

Granted, we should all strive to do as much as possible to prepare for old age, and many people have made enormous sacrifices in preparation for retiring. The hard truth is that some people are much better-positioned than others. Obvious examples include a public employee with a pension waiting for him at the end of his career, or a well-paid biotechnology worker with an employer that contributes 10 percent of every paycheck to her retirement savings account. These workers frequently also have employer-sponsored health insurance, which limits their out-of-pocket spending on medical care. This leaves more money for retirement saving than someone who pays their entire premium and has a $5,000 deductible.

Sure, we could all do a better job of planning out our careers when we’re first starting out. But my husband, as a Boston public school teacher, started accruing pension credits before he could’ve imagined ever getting old. He recently retired, and his pension, accumulated during 27 years of teaching, is making our life a lot easier.

Sure, we could all do a better job of planning out our careers when we’re first starting out. But my husband, as a Boston public school teacher, started accruing pension credits before he could’ve imagined ever getting old. He recently retired, and his pension, accumulated during 27 years of teaching, is making our life a lot easier.

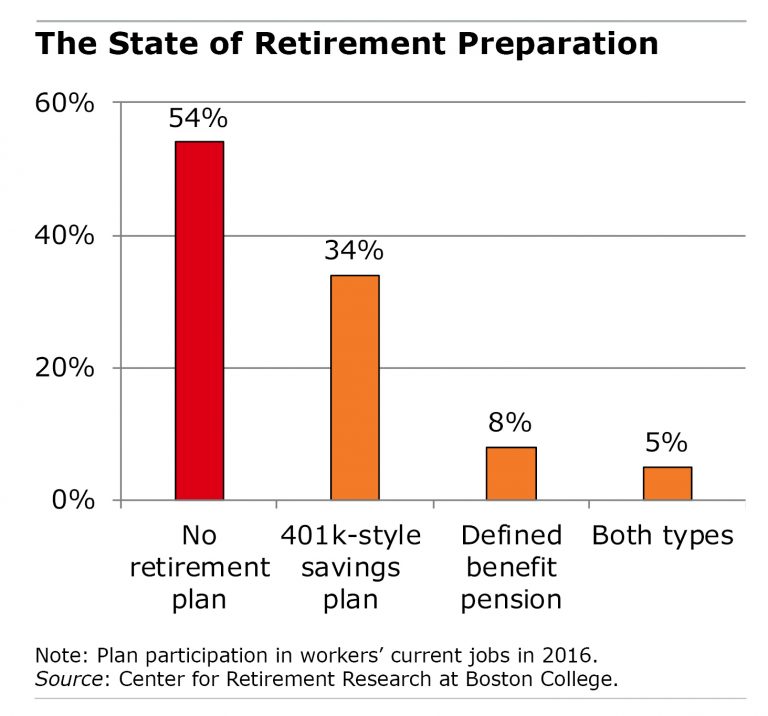

But pensions are on the wane in the private sector, and more than half of U.S. workers have neither a pension nor a 401(k) in their current job – this makes it pretty hard to save. IRAs are an option available to anyone, but human inertia makes that an imperfect solution to the problem, because people tend to procrastinate and don’t set them up. Further, working couples in which only one spouse has a 401(k) aren’t saving enough for both of them, one analysis found. …Learn More

January 14, 2020

Oddly, the Educated Pay Higher Fees

It’s smart to invest retirement savings in mutual funds that charge very low fees for one simple reason: the worker keeps more of his money and hands over less to Wall Street.

But in a study of people in their 50s and 60s who have retired or otherwise left federal employment, the people with the most education and the best scores on a standardized test were more likely to make what seems to be the wrong decision. Rather than keep their retirement funds in the government’s Thrift Savings Plan (TSP), which has extremely low fees, they transferred the money to much higher-fee IRAs operated by financial companies.

The $500 billion TSP – the world’s largest defined contribution retirement plan – is inexpensive in large part because it invests only in index mutual funds, which automatically track a variety of stock and bond market indexes and avoid the need to pay money managers to pick the investments. The annual fees for TSP’s index funds – known as expense ratios – are under 0.04 percent of the investor’s assets.

But over a 10-year period, about one fourth of the former federal employees rolled over the money saved during their careers into IRAs that typically had much higher expense ratios: 0.57 percent. On top of that, IRAs often charge additional fees for investment advice, pushing the potential total annual fees to well in excess of 1.5 percent. It’s possible that investing in an IRA could generate enough returns to make the extra fees worthwhile, but research has shown this is not the norm.

What explains the rollover decision? More educated people tend to have larger retirement account balances, raising the possibility that they were either seeking out financial advice or were targeted by advisors’ sales pitches. However, even among people with similar balances, those with more education were still more likely to roll over to IRAs.

It’s possible that they “perceive that they know what they’re doing” and want to take control of their investments “even when higher fees result,” the researchers said. …Learn More

December 31, 2019

Boomers Want to Make Retirement Work

The articles that our readers gravitated to over the course of this year provide a window into baby boomers’ biggest concerns about retirement.

Judging by the most popular blogs of 2019, they were very interested in the critical decision of when to claim Social Security and whether the money they have saved will be enough to last into old age.

Nearly half of U.S. workers in their 50s could potentially fall short of the income they’ll need to live comfortably in retirement. So people are also reading articles about whether to extend their careers and about other ways they might fill the financial gap.

Here is a list of 10 of our most popular blogs in 2019. Please take a look!

Half of Retirees Afraid to Use Savings

How Long Will Retirement Savings Last?

The Art of Persuasion and Social Security

Social Security: the ‘Break-even’ Debate

Books: Where the Elderly Find Happiness

Second Careers Late in Life Extend Work …Learn More

December 24, 2019

Happy Holidays!

Next Tuesday – New Year’s Eve – we’ll return with a list of some of our readers’ favorite blogs of 2019. Our regular featured articles will resume Thursday, Jan. 2.

Thank you for reading and posting comments on our retirement and personal finance blog. We hope you’ll continue to be involved in the new year. …

Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.