Posts Tagged "employers"

August 20, 2019

Modifying a Retirement Plan is Tricky

Employers beware: changing your retirement plan’s design can have unfortunate, unintended consequences for your employees.

That’s what happened to the Thrift Savings Plan (TSP) for federal workers, says a new study by a team of researchers for the NBER Retirement and Disability Research Center.

Like many private-sector savings plans, the $500 billion TSP – one of the nation’s largest retirement plans – has automatic enrollment. Federal employees can make their own decision about how much they want to save and, in a separate decision, how to invest their money. But if they don’t do anything, their employer will automatically do it for them.

In 2015, the TSP changed its automatic, or default, investment from a government securities fund to a lifecycle fund invested in a mix of stocks and bonds with the potential for higher returns than the government fund. However, the employer did not change the plan’s default savings rate for workers – 3 percent of their gross pay. (The government matches this contribution with a 3 percent contribution to employees’ accounts.)

After the TSP switched to the lifecycle fund, the new employees at one federal agency – the Office of Personnel Management – started saving less, the researchers said.

This probably occurred because, in passively accepting the TSP’s new lifecycle fund – a more appealing option than the old government securities fund – they were also passively accepting the relatively low default 3 percent contribution.

Employees seem to “make asset and contribution decisions jointly, rather than separately,” the researchers concluded. …Learn More

June 20, 2019

Index Fund Rise Coincides with 401k Suits

Employee lawsuits against their 401(k) retirement plans are grinding through the legal system, with mixed success. Many employers are beating them back, but there have also been some big-money settlements.

This year, health insurer Anthem settled a complaint filed by its employees for $24 million, Franklin Templeton Investments settled for $14 million, and Brown University for $3.5 million.

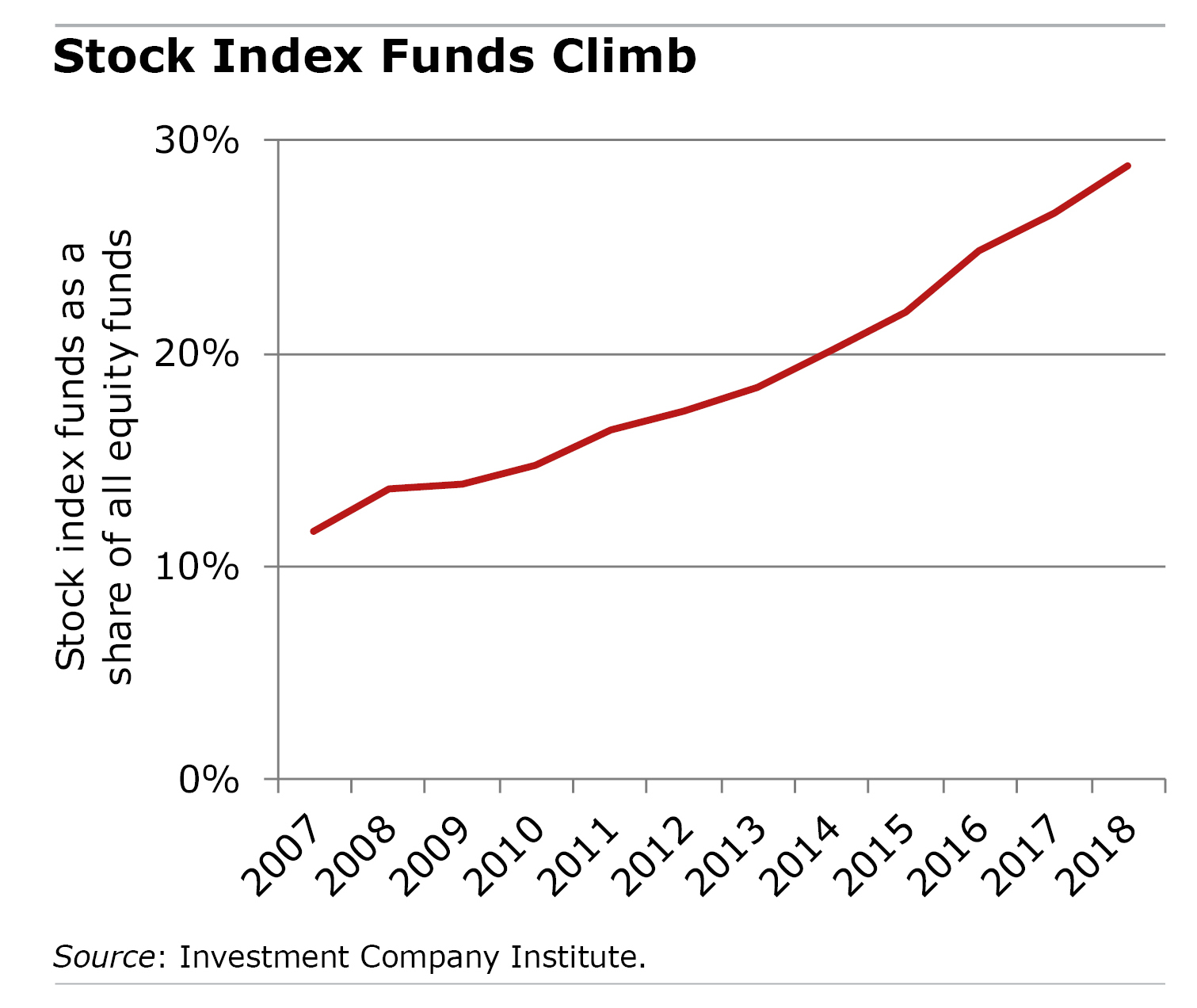

More 401(k) lawsuits were filed in 2016 and 2017 than during the 2008 financial crisis, and the steady drumbeat of litigation could be affecting how workers save and invest. For one thing, the suits have coincided with a dramatic increase in equity index funds, according to a report by the Center for Retirement Research. Last year, nearly one out of three U.S. stock funds were index funds, double the share 10 years ago.

Some see this change as positive. Many retirement experts believe that the best investment option for an inexperienced 401(k) investor is an index fund, which automatically tracks a specific stock market index, such as the S&P500. Federal law requires employers to invest 401(k)s for the “sole benefit” of their workers, and index funds usually charge lower fees and carry less risk of underperforming the market than actively managed funds – two issues at the heart of the lawsuits.

Some see this change as positive. Many retirement experts believe that the best investment option for an inexperienced 401(k) investor is an index fund, which automatically tracks a specific stock market index, such as the S&P500. Federal law requires employers to invest 401(k)s for the “sole benefit” of their workers, and index funds usually charge lower fees and carry less risk of underperforming the market than actively managed funds – two issues at the heart of the lawsuits.

To avoid litigation – and to comply with recent regulatory changes – employers are also becoming more transparent about the fees their workers pay to the 401(k) plan record keeper and to the investment manager. This transparency may have had a beneficial effect: lower mutual fund fees, which translate to more money in workers’ accounts when they retire. The average fund fee is about one-half of 1 percent, down from three-fourths of 1 percent in 2009, according to Morningstar.

In short, these lawsuits appear to be changing how people invest and how much they pay in fees for their 401(k)s. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.