Posts Tagged "healthcare"

September 27, 2018

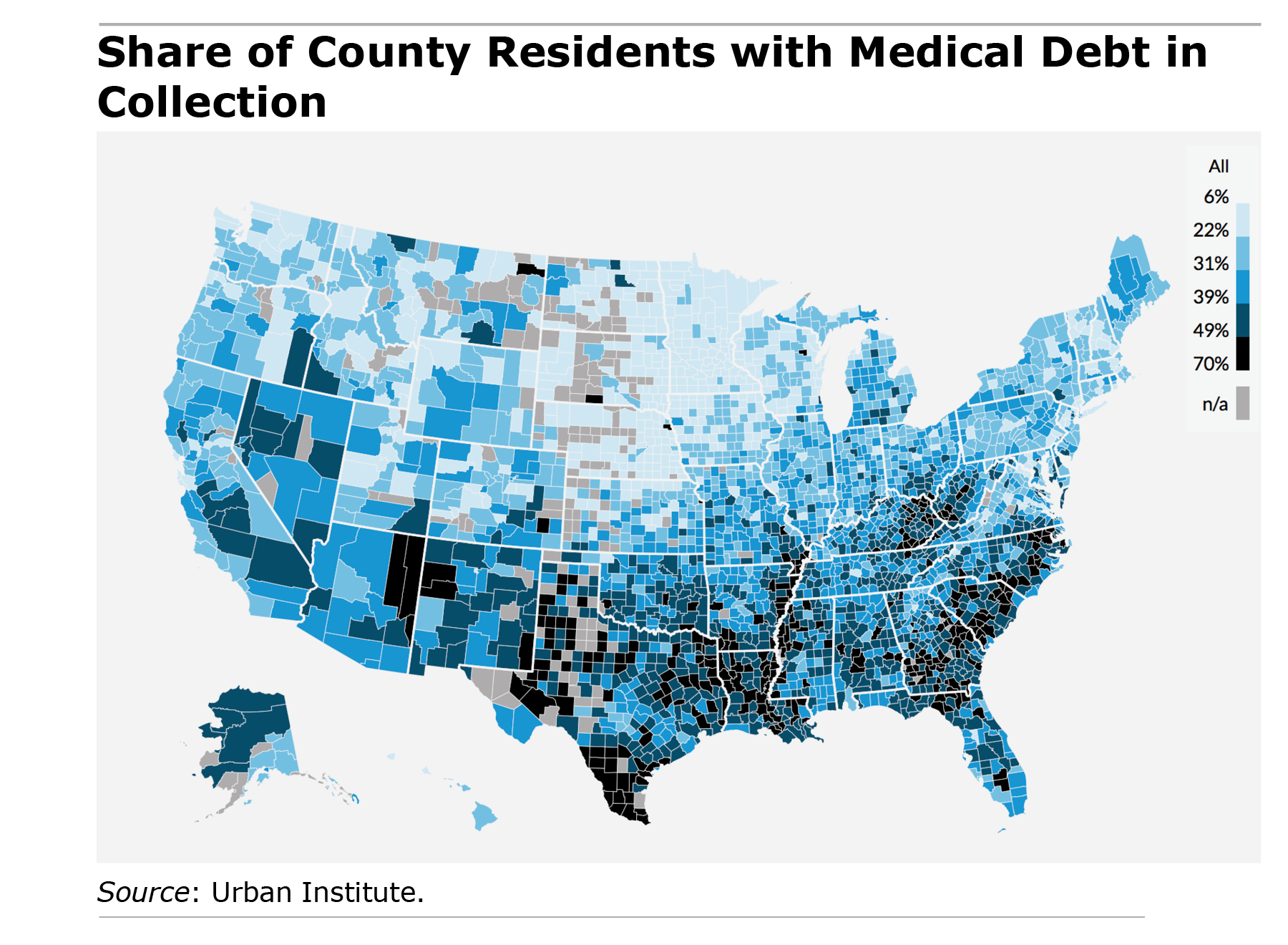

Medicaid Expansion Reduces Unpaid Debt

One in five Americans is burdened by unpaid medical bills that have been sent to a collection agency. Medical debt is the most common type of debt in collections.

This burden falls hardest on lower-paid people, who have little money to spare between paychecks. These are the same people the 2014 Medicaid expansion under the Affordable Care Act (ACA) was designed to help. Some 6.5 million additional low-income workers were getting insurance coverage just two years after Medicaid’s expansion, which increased the program’s income ceiling for eligibility in the states that chose to adopt the expansion.

The evidence mounts that this major policy has improved the precarious finances of vulnerable households.

The evidence mounts that this major policy has improved the precarious finances of vulnerable households.

A new study of the regions of the country with the largest percentage of low-income residents found that putting more people on Medicaid has reduced the number of unpaid bills of all kinds that go to collection agencies and cut by $1,000 the amounts that individuals had in collections.

The impact in states that did not expand Medicaid is apparent in Urban Institute data. Five of the 10 states with the highest share of residents owing money for medical bills – North Carolina, South Carolina, Oklahoma, Tennessee and Texas – decided against expanding their Medicaid-covered populations under the ACA option. About one in four of their residents have medical debt in collections.

That’s in contrast to Minnesota, which has one of the most generous Medicaid programs in the country and the lowest rate of medical debt collection of any state (3 percent of residents), said Urban Institute economist Signe-Mary McKernan.

“Past due medical debt is a big problem,” she said. “When [people] have high-quality health care, it makes a difference not only in their physical health but in their financial health.” …

Learn More

August 28, 2018

Medigap Premiums Differ by Thousands

- A 65-year-old woman in Houston can pay $5,300 a year for Medigap’s Plan C policy or she can buy a policy with exactly the same coverage from another insurance company for $1,700 a year.

- A 65-year-old Hartford, Connecticut, man can spend anywhere from $2,900 to $7,400 annually for the most popular and comprehensive Medigap policy – Plan F.

- The price disparity for Plan A for a 75-year-old man in Manchester, New Hampshire, is also large: anywhere from $1,820 to $6,301.

These are fairly typical of the enormous differences in the premiums that consumers across the country are paying for their Medigap policies.

The price disparities are “extraordinary and unable to be justified purely by the coverage that they’re offering,” said Gavin Magor, director of ratings for Weiss Ratings Inc., a consumer-oriented company that assesses insurance companies’ financial stability.

A nationwide analysis by Weiss shows that the premiums vary widely within each group of plans – Medigap Plans A, B, C through N – despite the fact that the coverage in each group is dictated by the federal government and does not change from one insurer to the next. Every company selling a Plan F policy, for example, must offer exactly the same coverage. (The exceptions are Massachusetts, Wisconsin, and Minnesota, where the states regulate their Medigap plans.)

If two people are buying a Chevrolet Camaro in Houston, “you would not expect one person to pay two or three times more than the other one,” Magor said.

Medigap is an added layer of insurance to supplement Medicare for people over 65. The additional coverage helps them with the copayments, deductibles, skilled nursing, and other charges that Medicare does not pay for.

Weiss supplied the data for this article by comparing Medigap premiums sold in each zip code and separately for men and women and for different age groups. The company based the analysis on premiums at more than 170 insurance companies.

There are a few viable explanations for the disparity in premiums. Urban and rural zip codes in the same state may be priced differently, in part because medical costs tend to be higher in the cities. And some insurers might be able to offer lower premiums, either because they are more efficient or are trying to be more price competitive to gain market share.

But Magor said that none of these explanations can fully account for the enormous price differences within zip codes. Many insurers are overcharging for their Medigap policies, he said.

A spokeswoman for America’s Health Insurance Plans, which represents health insurers, said she could not comment on Weiss’ information without the organization doing its own analysis of the data.

Paying too much for a Medigap plan can have a material impact on a retiree’s life. …

Learn More

June 21, 2018

Despite Medicare, Medical Expenses Bite

Medicare pays for the bulk of the medical care for Americans over 65, but a lot of their income is still eaten up by medical expenses.

The list of expenses is long. The lion’s share goes toward various insurance premiums – for Medicare Part B coverage, Part D prescription drug coverage, and supplemental insurance, whether Medigap, a Medicare Advantage plan, or employer health insurance for retirees. The remaining costs, for copayments and deductibles, are also significant.

These out-of-pocket costs, when added together, averaged about $4,300 annually per person, finds a new study by researchers Melissa McInerney, Matthew Rutledge, and Sara Ellen King of the Center for Retirement Research.

Out-of-pocket costs consume a third of the amount that retirees receive from Social Security, which is the most significant source of retirement income for a wide swath of the nation’s seniors, including many people in the middle-class. Half of seniors get at least half of all their income from the federal program.

The Medicare Part D prescription drug program has given some relief to retirees. After it became effective in 2006, the share of seniors’ income consumed by out-of-pocket costs declined slightly and then declined again after a follow-up reform of Part D began to close a big gap in drug coverage – known as the donut hole – in 2010. …Learn More

June 14, 2018

Health in Old Age: the Great Unknown

This cartoon, by Vancouver Sun cartoonist Graham Harrop, hits on one of retirees’ biggest mysteries: their future health.

This cartoon, by Vancouver Sun cartoonist Graham Harrop, hits on one of retirees’ biggest mysteries: their future health.

The elderly live with the anxiety of getting a grave illness that isn’t easy to fix, such as cancer or a stroke. And despite having Medicare insurance, they also have to worry how much it would cost them and whether they would run through all of their savings.

They’re right to worry. Health care costs increase as people age from their 50s into their 60s and 70s. About one in five baby boomers between 55 and 64 pays extraordinary out-of-pocket medical expenses in any given year. But by 75, the odds increase to one in four, according to a report summarizing the reasons that some seniors’ finances become fragile.

Large, unexpected medical expenses are one of two major financial shocks that threaten their security – widowhood is the other. A small and unlucky share of retirees will find it difficult to absorb a spike in their medical costs, forcing them to cut back on food or medications, the report said.

Harrop’s cartoon is the product of his cousin’s inspired suggestion that he fill a book with cartoons about the humorous accommodations made between couples who’ve lived together for decades. The book – “Living Together after Retirement: or, There’s a Spouse in the House” – reveals his personal knowledge of the subject. Harrop, who is 73, has lived with his partner, Annie, for more than 20 years.Learn More

May 31, 2018

Medicaid Now Critical to Aging Workers

For decades, the Medicaid program has subsidized health care for the poor, including retirees.

Yet, until recently, it largely excluded most working-age adults without disabilities due to a strict monthly income limit.

![]() All that changed in the 32 states and the District of Columbia that accepted the Affordable Care Act’s (ACA) option to expand their Medicaid coverage to low-income working people.

All that changed in the 32 states and the District of Columbia that accepted the Affordable Care Act’s (ACA) option to expand their Medicaid coverage to low-income working people.

In 2010, the ACA increased Medicaid’s income limits for people to qualify for the insurance. Today, working baby boomers, as well as younger workers, can qualify if their income is below 138% of federal poverty levels – or $1,396 per month for a single person and $1,892 for couples.

This joint federal-state program now completely or partially insures about one in six people approaching retirement age, according to a new report citing U.S. Census Bureau data.

The expansion is at least partly responsible for a striking improvement in one statistic: the uninsured rate for adults between ages 50 and 64 fell from 15.5 percent in 2012 to 9.1 percent in 2016. …Learn More

May 22, 2018

Squared Away at Year 7

Seven years ago this month, this personal finance and retirement blog debuted. How things have changed.

For one thing, back in 2011, a lot more people were reading blogs and newspapers on their clunky desktop computers. In recognition of the now-ubiquitous smart phone – more accurately, a computer that happens to have a phone – we just redesigned how Squared Away looks on phones to enlarge the type and make the articles easier to read. Our older readers will appreciate this update.

Year 7 is also an opportunity to restate the blog’s mission, which, frankly, was not fully refined in the early years. In some ways, our mission has not changed: we continue to emphasize retirement security and personal finance, with a bent toward the evidence-based research that provides a clearer understanding of the financial, economic, and behavioral issues that are critical to a high quality of life.

We regularly report on research by scholars around the country, including studies produced by members of the U.S. Social Security Administration’s Retirement Research Consortium: the NBER Retirement Research Center in Cambridge, Mass., the University of Michigan Retirement Research Center, and the Center for Retirement Research at Boston College, which also is the blog’s home.

But it’s natural for a new publication to find its sweet spot over time, and Squared Away is no different. One theme that has emerged very clearly is that the threads of retirement saving are shot through the fabric of our financial lives.

The predicament of Millennials is an obvious example. Immediately after beginning their careers, 20- and 30-somethings – so much more than their parents and grandparents – are under the gun to save for retirements that no longer are likely to include a pension. …Learn More

March 27, 2018

Boomers Do Retirement their Way

In the two years since starting a series of blogs, “Boomers: Rewriting Retirement,” I’ve profiled five willing baby boomers in various phases of retirement as they grapple with a variety of issues.

The individual profiles are again posted here, in the event one of them might be helpful to a reader who missed it the first time.

And we’re always looking for more guinea pigs, if anyone has an interesting story to tell!

Click on the links at the end of each headline:

- “A Familiar Dilemma: to Work or Retire.”

- “Finally retired. Now What?”

- “Caring for her elderly parents 24/7.”

- A Californian’s Retirement is Part-time.”

- “The Ultimate in Travel: Retiring Abroad.”

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.