Posts Tagged "IRA"

April 1, 2021

What the Research Can Tell us about Retiring

It’s difficult to envision what life will look like on the other side of the consequential decision to retire.

But research can help demystify what lies ahead – about the decision itself, the financial challenges, and even the taxes. Readers understand this, as evidenced by the most popular blog posts in the first three months of the year.

Here are the highlights:

The retirement decision. The article, “Retirement Ages Geared to Life Expectancy,” attracted the most reader traffic. Myriad considerations go into a decision to retire. But a sense of whether one might live a long time – because of good health or simply seeing that parents or neighbors are living unusually long – is a compelling reason to postpone retirement either to remain active or to build up one’s finances to fund a longer retirement.

A recent study found that as men’s life spans have increased, they have responded by remaining in the labor force longer, especially in areas of the country with strong job markets and more opportunity. This is also true, though to a lesser extent, for working women.

The planning. The second most popular blog was, “Big Picture Helps with Retirement Finances.” It described the success researchers have had with an online tool they designed, which shows older workers the impact on their retirement income of various decisions. When participants in the experiment selected when to start Social Security or how to withdraw 401(k) funds, the tool estimated their total retirement income. If they changed their minds, the income estimate would change.

The tool isn’t sold commercially. But it’s encouraging that researchers are looking for real-world solutions to the financial planning problem, since the insights from experiments like these often make their way into the online tools that are available to everyone.

The taxes. It’s common for a worker’s income to drop after retiring. So the good news shouldn’t be surprising in a study highlighted in a recent blog, “How Much Will Your Retirement Taxes Be?” Four out of five retired households pay little or no federal and state income taxes, the researchers found. But taxes are an important consideration for retirees who have saved substantial sums. …Learn More

February 25, 2020

Have You Misplaced a Retirement Plan?

Wouldn’t it be nice to find some money sitting in a long-forgotten retirement account somewhere?

It’s not hard for workers to lose track of an old account as they move from employer to employer, often across state lines. Each state government keeps a repository of unclaimed property – most have been doing this since the 1980s – and residents and former residents can check online through a simple name search in the state’s unclaimed-accounts database.

But not everyone takes the trouble to search for the money or is even aware it exists. So billions of dollars have accumulated nationwide in various types of unclaimed accounts, including retirement plans, insurance policies, trusts, and brokerage and bank accounts – so much so that firms have sprung up that will do the legwork required for individuals to claim their money. But little has been known about how much sits idle in unclaimed retirement accounts.

A new study estimates conservatively that about $38 million, accumulated over many years in some 70,000 retirement savings plans nationwide, had not yet been claimed in the states’ property accounts as of 2016. Most of these are 401(k)-style plans but they also include IRAs and pension checks.

The average account value is only about $550. But the largest ones are anywhere from $5,000 to $13,000, which could be meaningful to retirees who are struggling financially. …Learn More

January 14, 2020

Oddly, the Educated Pay Higher Fees

It’s smart to invest retirement savings in mutual funds that charge very low fees for one simple reason: the worker keeps more of his money and hands over less to Wall Street.

But in a study of people in their 50s and 60s who have retired or otherwise left federal employment, the people with the most education and the best scores on a standardized test were more likely to make what seems to be the wrong decision. Rather than keep their retirement funds in the government’s Thrift Savings Plan (TSP), which has extremely low fees, they transferred the money to much higher-fee IRAs operated by financial companies.

The $500 billion TSP – the world’s largest defined contribution retirement plan – is inexpensive in large part because it invests only in index mutual funds, which automatically track a variety of stock and bond market indexes and avoid the need to pay money managers to pick the investments. The annual fees for TSP’s index funds – known as expense ratios – are under 0.04 percent of the investor’s assets.

But over a 10-year period, about one fourth of the former federal employees rolled over the money saved during their careers into IRAs that typically had much higher expense ratios: 0.57 percent. On top of that, IRAs often charge additional fees for investment advice, pushing the potential total annual fees to well in excess of 1.5 percent. It’s possible that investing in an IRA could generate enough returns to make the extra fees worthwhile, but research has shown this is not the norm.

What explains the rollover decision? More educated people tend to have larger retirement account balances, raising the possibility that they were either seeking out financial advice or were targeted by advisors’ sales pitches. However, even among people with similar balances, those with more education were still more likely to roll over to IRAs.

It’s possible that they “perceive that they know what they’re doing” and want to take control of their investments “even when higher fees result,” the researchers said. …Learn More

November 5, 2019

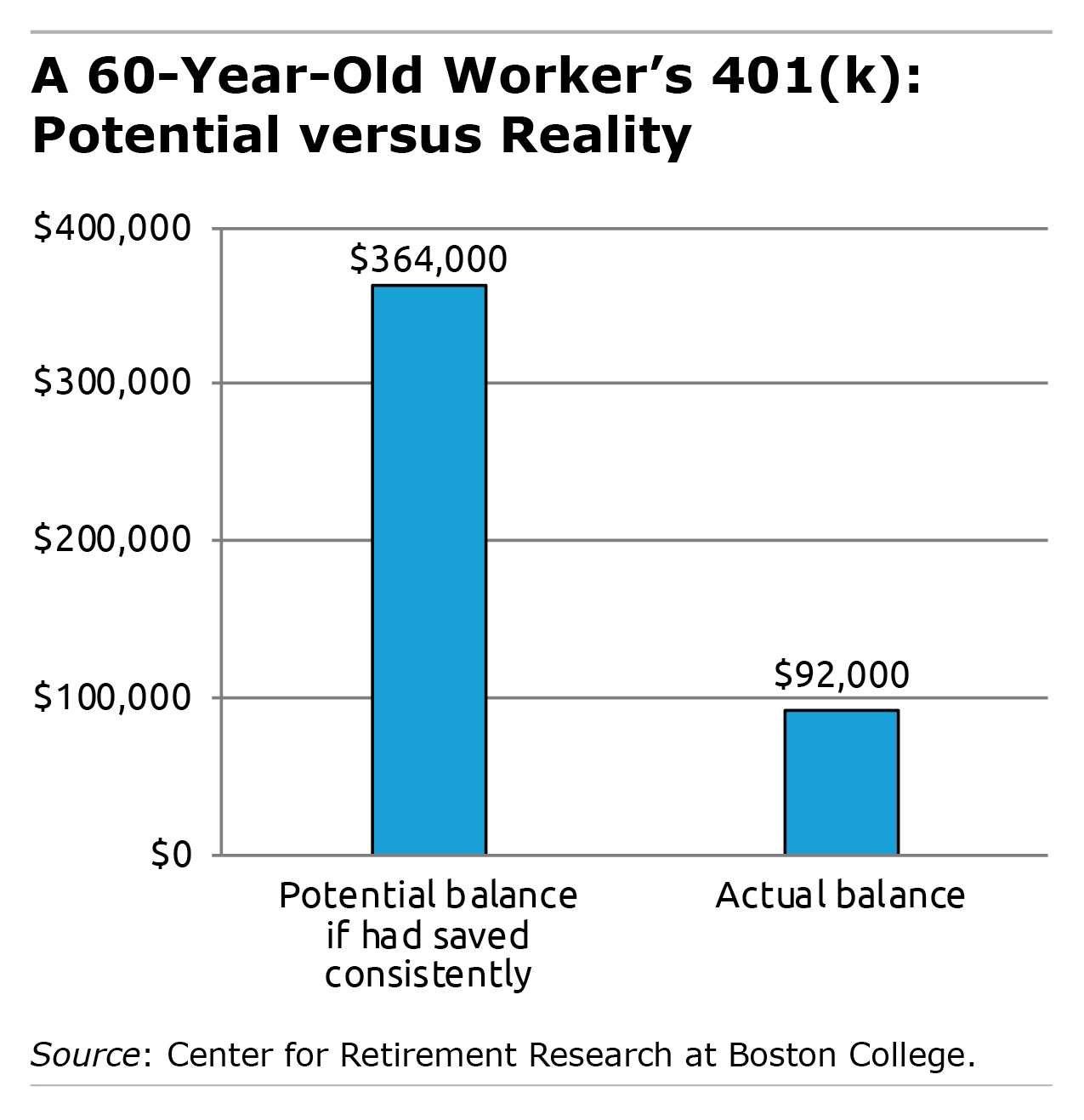

401k Balances are Far Below Potential

If a 60-year-old baby boomer started saving consistently at the beginning of his career back in the 1980s, he would have some $364,000 in his 401(k)s and IRAs today.

How much does he actually have? One-fourth of that, according to a new study from the Center for Retirement Research at Boston College (CRR).

One obvious explanation for the enormous gap is that the 401(k) system was in its infancy in the 1980s, and it took time for employers to widely adopt the plans and for young adults to get into the habit of saving for retirement.

Another likely reason is the large share of workers who do not have any type of employer-sponsored retirement plan. This coverage gap, which predates the introduction of 401(k)s, persists today and leaves about half of private-sector workers without a plan at any given point in time.

And this gap isn’t just a problem for baby boomers. A majority of young workers are not saving in a retirement plan, despite their advantage of having entered the labor force after the 401(k) system was more mature. …Learn More

October 29, 2019

People Tap IRAs After the Penalty Ends

Workers are apparently very eager to get their hands on the money in their retirement savings plans.

The evidence is the spike in withdrawals from IRA accounts that occurs soon after people turn 59½, the age at which the IRS’ 10 percent penalty on early withdrawals vanishes and is no longer a deterrent, according to a research study.

Average annual withdrawals from IRA accounts surge by about $1,965 to $3,540 – an 80 percent increase – after people cross the age 59½ threshold, according to the study, which was conducted for NBER’s Retirement Research Center by researchers at Stanford University, the University of Chicago, and the Federal Reserve Bank of Chicago.

Early withdrawals from tax-deferred retirement accounts – IRAs and 401(k)s – usually are not for frivolous reasons. This money tends to be tapped to ease financial hardships, such as unemployment, a disability, or a large, unexpected medical expense. But when older workers withdraw retirement funds – even for important matters – they may be chipping away at their financial security in old age. Withdrawals by high-income workers, on the other hand, will likely have little impact on their security.

The researchers analyzed taxpayer data from the IRS, which requires withdrawals to be reported at tax time. They compared withdrawals by people in the dataset for the two years before they turned 59½ with their withdrawals between 59½ and 60½.

While the penalty was in place, daily withdrawals were largely flat. But soon after people crossed the age 59½ threshold, withdrawals spiked before declining “to a new higher level than that of prior ages,” the researchers found. …Learn More

October 15, 2019

Does Increased Debt Offset 401k Savings?

Roughly half of U.S. employers with a 401(k) plan enroll their workers automatically, deducting money from their paychecks for retirement unless they explicitly opt out of this arrangement. This strategy is widely viewed as a good way to get people to save.

But auto-enrollment might not be as effective as it seems, if individuals are compensating for a smaller paycheck by borrowing more.

A new study of civilian employees of the U.S. Army used credit and payroll data to gauge whether debt increased for employees who were automatically enrolled in the federal government’s retirement savings plan. The researchers compared changes in debt levels for people hired after the government’s 2010 adoption of auto-enrollment with hires prior to 2010.

The good news is that since the broadest debt category, which includes high-rate credit cards, did not increase, it did not offset the employees’ accumulated contributions. Their credit reports showed no increase in financial distress either, the study concluded.

However, the findings for car and home loans were ambiguous, so auto-enrollment “may raise these latter types of debt,” said the researchers, who are affiliated with NBER’s Retirement and Disability Research Center.

If workers are, in fact, borrowing more, the question, again, is whether the new debt is offsetting the additional savings under auto-enrollment. Auto and home loans – in contrast to credit cards – are used to finance an asset that has long-term value. Whether these forms of debt improve or erode net worth depends on the asset’s value and whether the value rises (say, a house in a growing city) or falls (a car after it’s driven off the lot).

The researchers did not have access to data on federal workers’ assets, which they would need to see what’s happening to their net worth. This remains an important question for future research. …Learn More

September 26, 2019

Half of Retirees Afraid to Use Savings

For most retirees, figuring out how much money to withdraw from savings every year is a difficult-to-impossible math problem. But the issue goes much deeper: fears about what the future might bring make this decision overwhelming.

Extreme caution is a popular solution. A 2009 study estimated that by the time middle-income retirees are in their 80s, they still had not touched about three-fourths of their savings, and 2016 research found that retirees with substantial assets are the most reluctant spenders. Vanguard recently reported that retirees with very modest savings turn around and reinvest a third of the money they’re required to withdraw under IRS rules after age 70½.

People saved all of their lives to make sure they will enjoy retirement. So why are they so reluctant to spend the money for the purpose it was intended?

A 2018 study in the Journal of Personal Finance surveyed retirees to get a sense of the psychology behind their caution.

Half of the survey respondents agreed with this statement: “The thought of my retirement portfolio balance going down over time brings me discomfort, even if the decline in value is a result of me spending money on my retirement goals.”

And the people who agreed with this statement said they feel like they are not well prepared financially to retire – and this had nothing to do with how prepared they actually are. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.