Posts Tagged "IRS"

April 1, 2021

What the Research Can Tell us about Retiring

It’s difficult to envision what life will look like on the other side of the consequential decision to retire.

But research can help demystify what lies ahead – about the decision itself, the financial challenges, and even the taxes. Readers understand this, as evidenced by the most popular blog posts in the first three months of the year.

Here are the highlights:

The retirement decision. The article, “Retirement Ages Geared to Life Expectancy,” attracted the most reader traffic. Myriad considerations go into a decision to retire. But a sense of whether one might live a long time – because of good health or simply seeing that parents or neighbors are living unusually long – is a compelling reason to postpone retirement either to remain active or to build up one’s finances to fund a longer retirement.

A recent study found that as men’s life spans have increased, they have responded by remaining in the labor force longer, especially in areas of the country with strong job markets and more opportunity. This is also true, though to a lesser extent, for working women.

The planning. The second most popular blog was, “Big Picture Helps with Retirement Finances.” It described the success researchers have had with an online tool they designed, which shows older workers the impact on their retirement income of various decisions. When participants in the experiment selected when to start Social Security or how to withdraw 401(k) funds, the tool estimated their total retirement income. If they changed their minds, the income estimate would change.

The tool isn’t sold commercially. But it’s encouraging that researchers are looking for real-world solutions to the financial planning problem, since the insights from experiments like these often make their way into the online tools that are available to everyone.

The taxes. It’s common for a worker’s income to drop after retiring. So the good news shouldn’t be surprising in a study highlighted in a recent blog, “How Much Will Your Retirement Taxes Be?” Four out of five retired households pay little or no federal and state income taxes, the researchers found. But taxes are an important consideration for retirees who have saved substantial sums. …Learn More

January 2, 2020

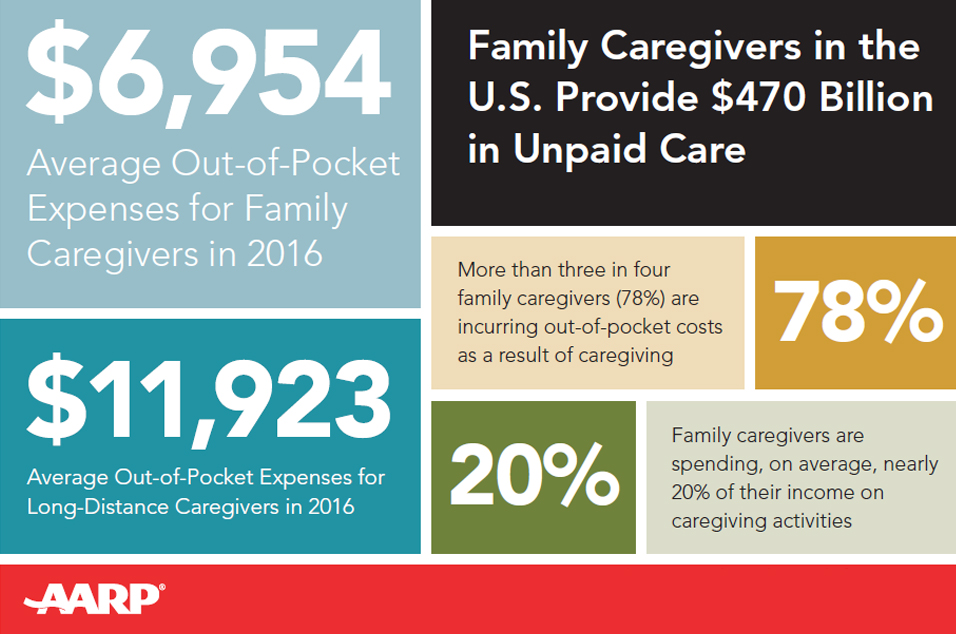

States Give Financial Help to Caregivers

On Jan. 1, Arizona residents caring for elderly or disabled family members became eligible for up to a $1,000 reimbursement from the state for expenses incurred in their caregiving responsibilities.

This is a trial program and the legislature allocated very little money – $1 million over two years – in a state with an estimated 800,000 residents caring for a disabled adult over 18.

But it’s a start.

Caregivers “aren’t asking for everything. They’re asking for a little bit to make their lives better,” said Elaine Ryan, vice president of government affairs for AARP, which has been on the forefront of advocating for such policies at the state level. “That’s the least we can do.”

Arizona’s program would defray a portion of caregivers’ spending. For older family members, this would cover technologies to aid older family members, such as hearing aids or computer programs, or shower grab bars and wheelchair ramps.

Like Arizona, state governments around the country, as laboratories for policy experimentation, have passed a hodgepodge of programs to support caregivers. Other bills approved in recent years range from New Jersey’s tax credit for military families caring for wounded veterans to Oregon’s paid family leave program for workers taking care of aging spouses, parents and grandparents.

The programs are a tacit acknowledgment of the enormous financial strain caregivers face – a strain that is only expected to grow and, increasingly, to affect Millennials as their baby boomer parents age.

However, it’s not easy to pass bills that require states to approve financial assistance or tax credits, because the work done quietly by family caregivers is often invisible and under-appreciated by the general public and federal and state legislators. …Learn More

November 14, 2019

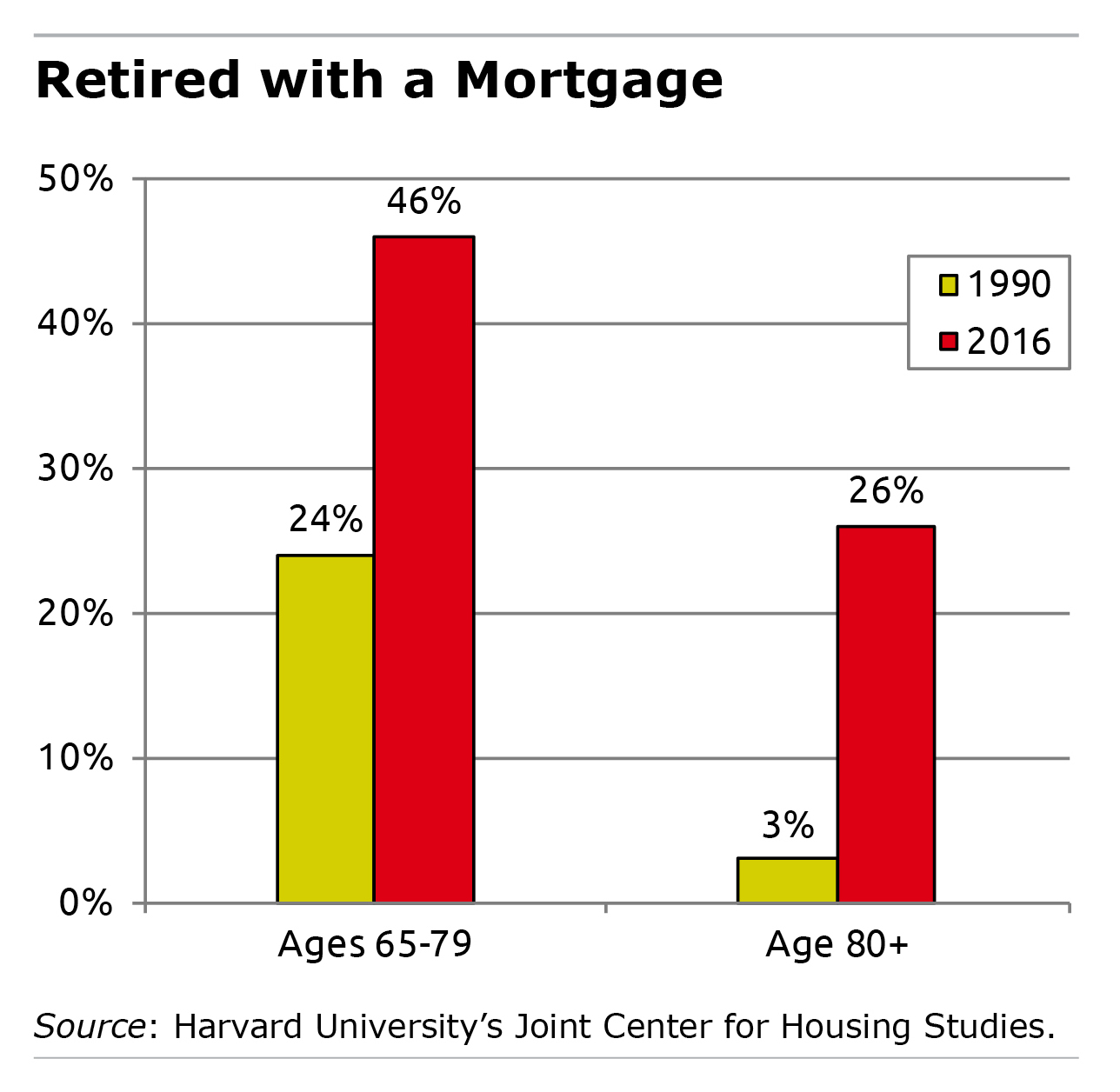

More Retirees Today Have a Mortgage

In one significant way, retirement is materially different than it used to be: far more retirees are still trying to pay off their houses.

Thirty years ago, just one of every four homeowners in their late 60s to late 70s still had a mortgage – today, nearly half do. Once people hit 80, mortgages used to be extremely rare – only 3 percent had them. Today, it’s one in four, Harvard’s Joint Center for Housing Studies recently reported.

Thirty years ago, just one of every four homeowners in their late 60s to late 70s still had a mortgage – today, nearly half do. Once people hit 80, mortgages used to be extremely rare – only 3 percent had them. Today, it’s one in four, Harvard’s Joint Center for Housing Studies recently reported.

Retiree’s financial condition depends on much more than how much they spend on housing – in particular the size of their retirement savings accounts and Social Security checks. But rent or a mortgage payment is typically the largest item in the monthly budget. Being free of both can be a significant boost to one’s standard of living in retirement.

Jennifer Molinsky, a senior research associate at Harvard’s housing center, described several developments over the past three decades that may explain the dramatic increase in the share of retirees with mortgages.

First, she said, Americans today “seem to have less aversion to debt” than the generation that grew up after the Great Depression and was instilled with frugality. Although consumer debt levels always ebb and flow with the economy’s cycles, total debt as a percentage of disposable income is significantly higher today than it was in the 1990s. The 1986 tax reform act also made mortgages a more attractive form of debt to hold. The reform eliminated the income tax deductions for interest on credit cards and other types of consumer debt, with one exception: mortgage interest.

Having a mortgage isn’t necessarily a bad thing. Mortgage rates have fallen dramatically in recent decades. Many retirees who are still making monthly mortgage payments were able to reduce the payments by refinancing old, partially paid off mortgages into new 30-year loans with lower interest rates.

But another factor that may have pushed up the share of retirees with mortgages has been the long-term run-up in house prices, relative to earnings, which makes it increasingly difficult to pay off a house before retiring. In the late 1980s and early 1990s, house prices were about three times the typical household’s earnings, according to the housing center. Today, prices are more than four times earnings. …Learn More

October 29, 2019

People Tap IRAs After the Penalty Ends

Workers are apparently very eager to get their hands on the money in their retirement savings plans.

The evidence is the spike in withdrawals from IRA accounts that occurs soon after people turn 59½, the age at which the IRS’ 10 percent penalty on early withdrawals vanishes and is no longer a deterrent, according to a research study.

Average annual withdrawals from IRA accounts surge by about $1,965 to $3,540 – an 80 percent increase – after people cross the age 59½ threshold, according to the study, which was conducted for NBER’s Retirement Research Center by researchers at Stanford University, the University of Chicago, and the Federal Reserve Bank of Chicago.

Early withdrawals from tax-deferred retirement accounts – IRAs and 401(k)s – usually are not for frivolous reasons. This money tends to be tapped to ease financial hardships, such as unemployment, a disability, or a large, unexpected medical expense. But when older workers withdraw retirement funds – even for important matters – they may be chipping away at their financial security in old age. Withdrawals by high-income workers, on the other hand, will likely have little impact on their security.

The researchers analyzed taxpayer data from the IRS, which requires withdrawals to be reported at tax time. They compared withdrawals by people in the dataset for the two years before they turned 59½ with their withdrawals between 59½ and 60½.

While the penalty was in place, daily withdrawals were largely flat. But soon after people crossed the age 59½ threshold, withdrawals spiked before declining “to a new higher level than that of prior ages,” the researchers found. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.