Posts Tagged "manage money"

February 25, 2016

Home Equity: a Retirement Resource

The National Council on Aging (NCOA) has redesigned its website providing information for “house rich but cash poor” older people who want to think about tapping their home equity.

Home equity – the house’s market value minus the amount owed on the mortgage – remains a largely unused source of income that many older Americans could be putting toward their medical care or to improve their lives.

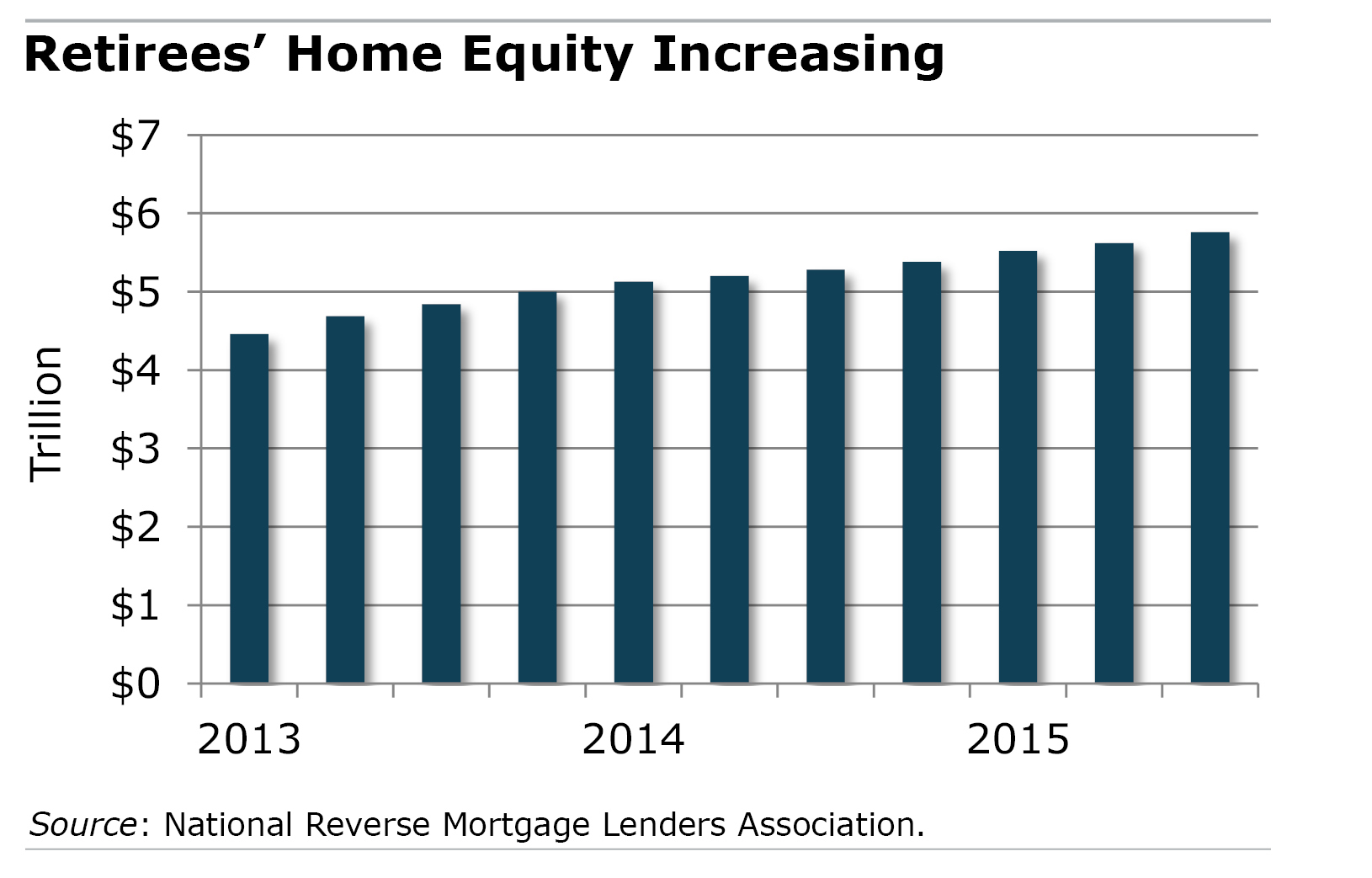

Home equity held by Americans age 62 and over reached $5.76 trillion last year – an increase of nearly 30 percent since 2013. A marker of how much of this retirement resource remains untapped is the small number of federally insured reverse mortgages – about 50,000 – that seniors take out every year against the value of their home equity. Reverse mortgages, which are available to homeowners at age 62, are equity loans that do not have to be repaid until the senior permanently leaves their home. …Learn More

Home equity held by Americans age 62 and over reached $5.76 trillion last year – an increase of nearly 30 percent since 2013. A marker of how much of this retirement resource remains untapped is the small number of federally insured reverse mortgages – about 50,000 – that seniors take out every year against the value of their home equity. Reverse mortgages, which are available to homeowners at age 62, are equity loans that do not have to be repaid until the senior permanently leaves their home. …Learn More

February 11, 2016

More Parents Split Bequests Unequally

As the American family becomes increasingly complex, so do parents’ wills.

The result has been a dramatic increase over the past two decades in the share of wills in which parents distribute their estate’s assets unequally among their genetic offspring and stepchildren.

New research, based on surveys of older Americans, finds that about one-third of parents today do not distribute their assets equally. The reasons range from the greater incidence of divorce and the inherent disadvantage of being a stepchild to the fact that some children naturally take on the role of caring for their aging parents. With parents now living longer and needing more care, children may receive compensation in the will for providing that care.

New research, based on surveys of older Americans, finds that about one-third of parents today do not distribute their assets equally. The reasons range from the greater incidence of divorce and the inherent disadvantage of being a stepchild to the fact that some children naturally take on the role of caring for their aging parents. With parents now living longer and needing more care, children may receive compensation in the will for providing that care.

About 42 percent of older parents have not written a will, though it’s unclear why, according to the study. But when there is a will, here is how complexity affects the distribution of bequests, based on the research findings: …Learn More

February 9, 2016

Could Social Security Statement Do More?

Two out of three working Americans grade their retirement readiness at no better than a “C.”

So how about using the Social Security Statement that lands in their mailboxes, grabbing their attention, to spur them to action?

The statement is already valued by millions of Americans. A survey funded by the U.S. Social Security Administration (SSA) found that people who received statements were “dramatically” more knowledgeable about their basic pension benefits than people who had already retired when SSA started mailing them out in the mid-1990s.

Social Security is the nation’s most important source of retirement income, and the information in the statements is essential to most workers’ retirement planning. Mailed out before every fifth birthday – 25, 30, 35, etc. – and annually at age 60, the statement provides estimates of each worker’s future benefits at three different claiming ages: 62, when they have access to their smallest monthly benefit; the “full retirement age”; and 70, when workers receive their highest monthly benefit. It clearly lays out how much workers can increase their monthly retirement income by delaying when they start collecting their benefits. …Learn More

February 4, 2016

U.S. Millionaires: a Racial Breakdown

This video examines wealth through the prism of race.

It compares the share of the nation’s African-American, Hispanic, Asian-American and white populations who have net worth exceeding $1 million; net worth equals financial and other assets minus mortgages and other debts. If the fact that there is a racial divide isn’t surprising, the magnitude of it might be.

Other factors also have an enormous influence over who gets rich, and understanding this becomes increasingly important amid rising inequality. The biggest determinant of wealth is whether our parents are rich, as recent research has shown. Age and education are also crucial. That’s because older people have more time to save and accumulate wealth, and a college education typically leads to jobs that can add an estimated $1 million to the total amount that a worker earns over a lifetime.

But even when the data are sliced by age and education, there are deep economic inequities in our diverse society, as this video produced by Bloomberg Business shows.Learn More

February 2, 2016

No-Free-Lunch Seminars for Seniors

Economists like to joke about free lunches. The subtext is that there’s a cost to everything.

A free lunch is also literally how high-pressure financial companies sometimes lure older Americans into a room to hear their investment pitches. The FINRA Investor Education Foundation says some 6 million older Americans have attended seminars in return for a free lunch. Every year, my mother’s retirement community outside of Orlando hosts a handful of these seminars, which are presented by financial firms, insurance companies, and even funeral homes.

FINRA warns that they can pressure seniors into making “unsuitable, even fraudulent investments.” The above FINRA video explains what’s behind the free-lunch presentations and proposes some questions that people can ask to determine the legitimacy of what’s being sold.

But it’s probably better to do what my mom does: find something fun to do instead.Learn More

January 28, 2016

Personal Finance Info – now in Spanish

The wealth of good financial information available from government, university, and non-profit organizations is an antidote to the television and Internet advertisements selling financial products. Squared Away regularly compiles these resources for our readers’ benefit. This newest installment starts with some that are available in Spanish for the nation’s growing Hispanic population:

- The FINRA Investor Education Foundation translated its short video about why people make bad financial decisions into Spanish. “Pensando Dinero: la psicología detrás de nuestras mejores y peores decisiones financieras” – or “Thinking Money” – explores how emotions get in the way of common sense when making decisions about money. Several other FINRA resources also in Spanish include a glossary of online financial publications and a video about financial fraud. (“Pensando Dinero” is based on a documentary produced for public television; a free DVD of the English-language documentary is also available.)

- “Thinking Fast and Slow” by Daniel Kahneman was an international bestseller about behavioral economics. To explore another insider’s take on this field, read what one of the field’s founders says about it. Richard Thaler’s latest book, “Misbehaving,” will be published in paperback in May. A New York Times review called it “a sly and somewhat subversive history of his profession.”

- In just two years, the housing boom taking place in many parts of the country has added

$1 trillion to the value of home equity held by people ages 62 and older, reports the National Reverse Mortgage Lenders Association. For retirees wondering whether it’s appropriate to turn some of their equity into income, the Center for Retirement Research at Boston College, which supports this blog, has produced a booklet on ways retirees can use their home equity, including through reverse mortgages. The online version is free, and a paper version costs a whopping $2.75.

January 14, 2016

Policy Reduces Elderly Women’s Incomes

Poverty is the scourge of women in old age.

This problem was aggravated, according to a new study, when older workers started claiming their Social Security benefits sooner after the earnings test was lifted in 2000 for those who reach the program’s full retirement age.

The earnings test withholds benefits from older workers earning more than a specified amount – the withheld benefits are returned later, in the form of an increase in monthly Social Security checks. But the earnings test is, nevertheless, often viewed as a tax in the mistaken belief that these benefits are never restored.

Researchers at the U.S. Treasury Department and the University of California at Irvine found that people reacted in one of two ways to lifting the earnings test, both based on the misperception it’s a tax. One response was to work longer – as Congress intended – under the logic that benefits would no longer be unduly “taxed” after workers entered their late 60s. The second and more common response was to claim benefits earlier than one would have prior to the policy change, when workers perceived that delayed claiming was the way to avoid this “tax.”

The earnings test remains in place for beneficiaries younger than the full retirement age – 66 for most boomers. However, the researchers analyzed a broader age range of workers – 62 to 70; even those who haven’t yet reached their full retirement age might change their behavior in anticipation they will soon reach it, and the test will no longer apply to them.

Earlier claiming by men and women, which results in smaller monthly Social Security checks, has fallen especially hard on elderly widows. After a husband dies, the two benefit checks coming into the house are reduced to one. Although widows receive the larger of the couple’s two checks – typically the husband’s – it may not be sufficient to maintain her standard of living. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.