Posts Tagged "retirement"

November 7, 2019

A Brighter Future for a Graying Workforce

Perceptions of older workers haven’t caught up with the reality of their increasingly prominent role in the labor force.

The federal Administration for Community Living reports that the U.S. population over age 60 has surged nearly 40 percent in just the past decade. By 2030, retirees will outnumber children for the first time in history, the U.S. Census Bureau predicts. The world population is on a similar path.

But in the face of this significant demographic shift, discriminatory views of older people persist in obvious and subtle ways. This discrimination colors coworkers’ beliefs about, among other things, older workers’ mental ability, efficiency, and competence on the job, according to one international review of studies on aging.

When people think about the future, “they fail to appreciate the potential that older workers present as workers and consumers,” Paul Irving, an expert on aging, writes in a special November edition of the Harvard Business Review exploring issues relevant to our aging workforce.

Research backs him up. Older people are living longer than past generations, which gives them more capacity to extend their work lives. They’re also generally healthier and enjoy more disability-free years, thanks to innovations like cataract surgery to restore their vision.

But ageism’s consequences are still apparent in the workplace. An Urban Institute report said that older workers, for a variety of reasons, are frequently pushed or nudged out of a long-term job at some point late in their careers. Some are forced into early retirement. And for those who do find another job, the new opportunities, while less stressful, are often a step down in terms of prestige and pay.

Irving, who is chairman of the Milken Institute’s Center for the Future of Aging, wants to chart a more hopeful path for our graying U.S. workforce, one that views it as an opportunity – rather than a looming crisis. …Learn More

November 5, 2019

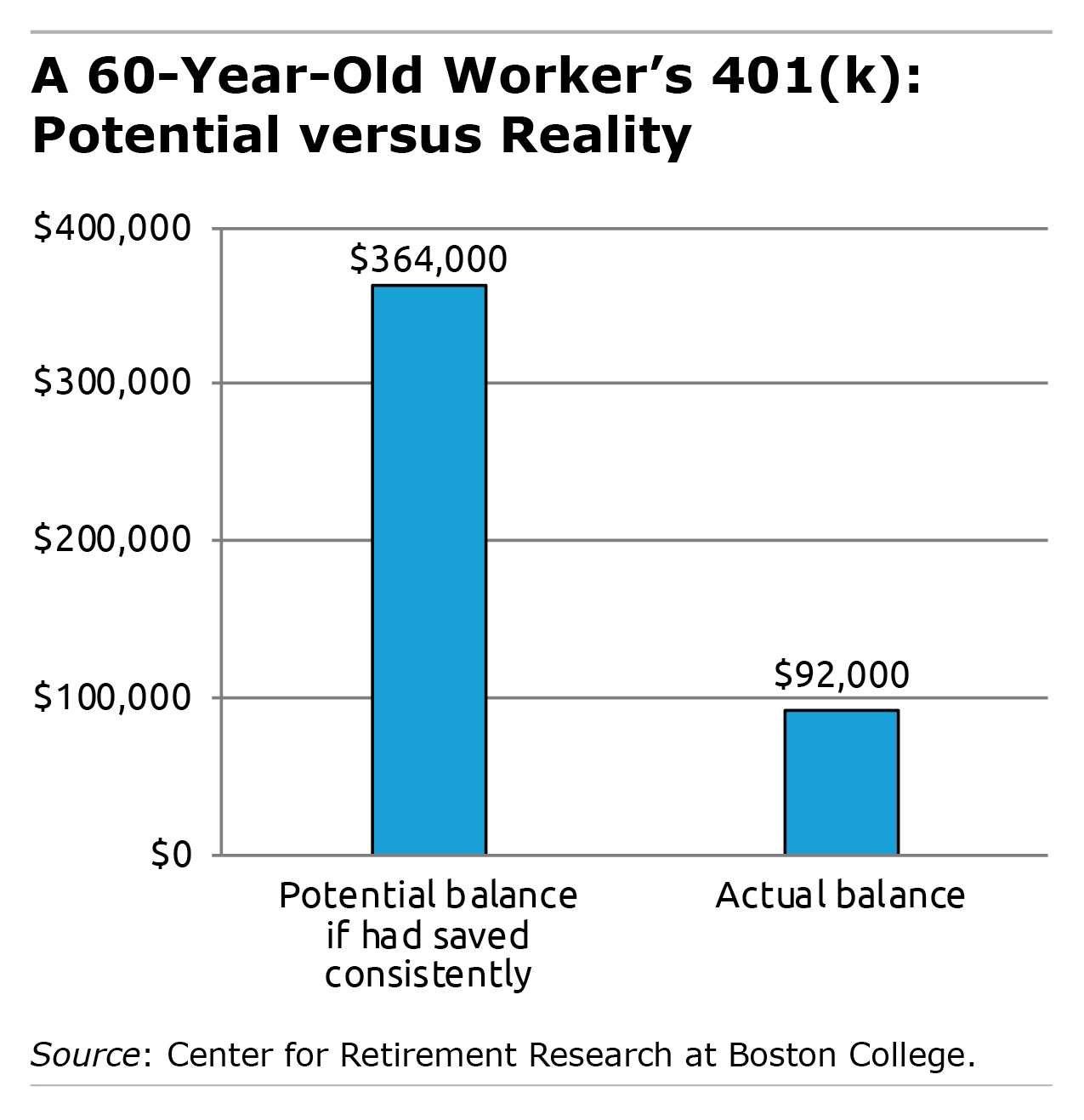

401k Balances are Far Below Potential

If a 60-year-old baby boomer started saving consistently at the beginning of his career back in the 1980s, he would have some $364,000 in his 401(k)s and IRAs today.

How much does he actually have? One-fourth of that, according to a new study from the Center for Retirement Research at Boston College (CRR).

One obvious explanation for the enormous gap is that the 401(k) system was in its infancy in the 1980s, and it took time for employers to widely adopt the plans and for young adults to get into the habit of saving for retirement.

Another likely reason is the large share of workers who do not have any type of employer-sponsored retirement plan. This coverage gap, which predates the introduction of 401(k)s, persists today and leaves about half of private-sector workers without a plan at any given point in time.

And this gap isn’t just a problem for baby boomers. A majority of young workers are not saving in a retirement plan, despite their advantage of having entered the labor force after the 401(k) system was more mature. …Learn More

October 31, 2019

Boomers at 80: Housing Issues to Grow

The baby boom generation is continuing to work its way up the age ladder. The number of Americans over 80 will more than double to nearly 18 million over the next two decades.

And that’s partly because baby boomers are healthier and are living longer – they are also enjoying more of their retirement years free of disability than previous generations. But unfortunately, boomers can’t avoid the inevitability of their growing vulnerabilities and the impact this will have on their day-to-day lives. A new report by Harvard’s Joint Center for Housing Studies makes some sobering predictions about the issues the oldest retirees can expect to face in the future, from widening income inequality to more people living alone and in isolation.

The findings, taken together, point to a range of potential trouble spots revolving around housing our aging population.

- As people get old, their spouses die, their bank accounts dwindle, and their rents keep rising. For these and other reasons, housing creates more of a cost burden at 80 than at 65. The Harvard housing center defines someone as cost-burdened if they spend more than 30 percent of their income on housing. Today, nearly 60 percent of households over 80 fit this definition, and their absolute numbers will increase as more baby boomers reach that age. One place the financial strain shows up is food budgets: retirees who spend disproportionate amounts on housing spend half as much on food as people whose housing costs are under control. …

October 29, 2019

People Tap IRAs After the Penalty Ends

Workers are apparently very eager to get their hands on the money in their retirement savings plans.

The evidence is the spike in withdrawals from IRA accounts that occurs soon after people turn 59½, the age at which the IRS’ 10 percent penalty on early withdrawals vanishes and is no longer a deterrent, according to a research study.

Average annual withdrawals from IRA accounts surge by about $1,965 to $3,540 – an 80 percent increase – after people cross the age 59½ threshold, according to the study, which was conducted for NBER’s Retirement Research Center by researchers at Stanford University, the University of Chicago, and the Federal Reserve Bank of Chicago.

Early withdrawals from tax-deferred retirement accounts – IRAs and 401(k)s – usually are not for frivolous reasons. This money tends to be tapped to ease financial hardships, such as unemployment, a disability, or a large, unexpected medical expense. But when older workers withdraw retirement funds – even for important matters – they may be chipping away at their financial security in old age. Withdrawals by high-income workers, on the other hand, will likely have little impact on their security.

The researchers analyzed taxpayer data from the IRS, which requires withdrawals to be reported at tax time. They compared withdrawals by people in the dataset for the two years before they turned 59½ with their withdrawals between 59½ and 60½.

While the penalty was in place, daily withdrawals were largely flat. But soon after people crossed the age 59½ threshold, withdrawals spiked before declining “to a new higher level than that of prior ages,” the researchers found. …Learn More

October 24, 2019

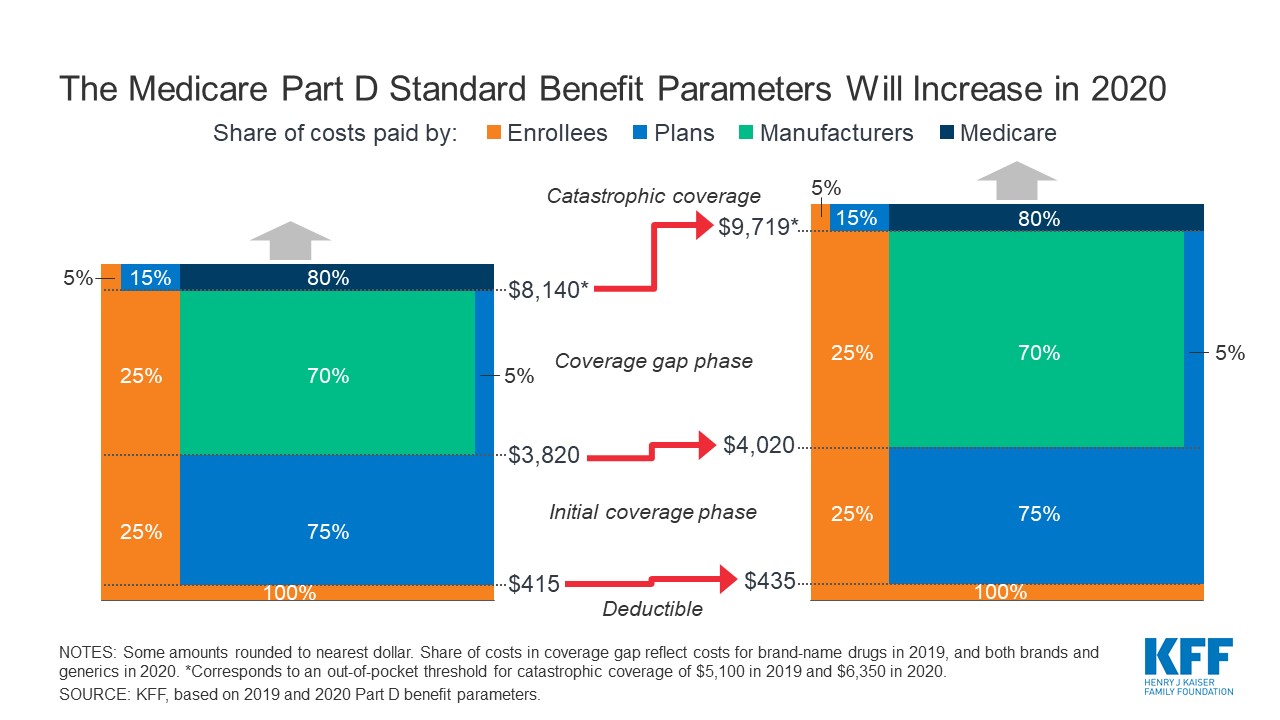

Part D Cost for Brand Name Drugs Rising

Reforms to Medicare Part D under the Affordable Care Act brought significant relief to retirees by reducing the share of medication costs they must pay out of their own pockets.

But with the healthcare reform now nearly a decade old, other developments have taken over that will drive up drug costs for the most vulnerable retirees – the biggest users of expensive brand name drugs. Although only a few million people will be affected, they are already saddled with the highest spending burden.

This vulnerable group could get some help from Congress. There is bipartisan support for placing an absolute limit on how much Part D policyholders must pay in total for their prescriptions, said Juliette Cubanski, associate director of the Medicare policy program at the Kaiser Family Foundation.

“That’s a positive development,” she said, “but there are also several areas of disagreement in the legislation being considered on the House and Senate sides.”

Under the Affordable Care Act (ACA), retirees are required to pay 25 percent of their total drug costs up to the annual threshold that qualifies them for catastrophic coverage – this dollar threshold is the total of their own payments plus the price discounts from manufacturers of brand name drugs. The upshot in 2020 for retirees is that those with the highest need could spend about $375 more out of their own pockets before they enter Part D’s less-onerous catastrophic coverage phase, according to a Kaiser analysis. And that’s just the increase for next year – their outlays will rise over the next decade.

Once retirees enter the catastrophic phase, they are protected, because Medicare begins picking up the vast majority of the tab. But out-of-pocket costs are rising because the ACA’s controls on the spending threshold they must cross to qualify for catastrophic coverage have ended. …Learn More

October 22, 2019

Most Data Sets Agree on Retiree Income

What kind of financial shape are retirees in?

A 2017 study refocused attention on this old question, and it has taken on greater urgency as more and more baby boomers retire.

The study looked at the accuracy of the U.S. Census Bureau’s Current Population Survey (CPS) and confirmed earlier research showing that it dramatically under-estimates retirees’ income. The under-reporting in the CPS could raise concerns about the accuracy of other surveys that paint a less-than-rosy picture of retirement life.

To get to the bottom of things, the Center for Retirement Research (CRR) dug into other standard sources of survey data on retired households so they could be compared with CPS data. They found that the income estimates in the CPS were much lower than the others and clearly the outlier – the other four data sets roughly agreed on how much income retirees have.

The CRR researchers then selected one of the reliable sources of income data – the Health and Retirement Study (HRS) – to assess how retirees are faring. They concluded that around half of over-65 households may be experiencing difficulty maintaining the standard of living they enjoyed while they were working. The researchers based this on the rule of thumb that they need about 75 percent of their past employment earnings.

To be sure, every survey has its strengths and shortcomings, because they rely on what people say they are getting from their Social Security, retirement plans, and investments. …Learn More

September 26, 2019

Half of Retirees Afraid to Use Savings

For most retirees, figuring out how much money to withdraw from savings every year is a difficult-to-impossible math problem. But the issue goes much deeper: fears about what the future might bring make this decision overwhelming.

Extreme caution is a popular solution. A 2009 study estimated that by the time middle-income retirees are in their 80s, they still had not touched about three-fourths of their savings, and 2016 research found that retirees with substantial assets are the most reluctant spenders. Vanguard recently reported that retirees with very modest savings turn around and reinvest a third of the money they’re required to withdraw under IRS rules after age 70½.

People saved all of their lives to make sure they will enjoy retirement. So why are they so reluctant to spend the money for the purpose it was intended?

A 2018 study in the Journal of Personal Finance surveyed retirees to get a sense of the psychology behind their caution.

Half of the survey respondents agreed with this statement: “The thought of my retirement portfolio balance going down over time brings me discomfort, even if the decline in value is a result of me spending money on my retirement goals.”

And the people who agreed with this statement said they feel like they are not well prepared financially to retire – and this had nothing to do with how prepared they actually are. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.