Posts Tagged "retirement"

August 15, 2019

Walk? Yes! But Not 10,000 Steps a Day

A few of my friends who’ve recently retired decided to start walking more, sometimes for an hour or more a day.

Becoming sedentary seems to be a danger in retirement, when life can slow down, and medical research has documented the myriad health benefits of physical activity. To enjoy the benefits from walking – weight loss, heart health, more independence in old age, and even a longer life – medical experts and fitness gurus often recommend that people shoot for 10,000 steps per day.

But what’s the point of a goal if it’s unrealistic? A Centers for Disease Control study that gave middle-aged people a pedometer to record their activity found that “the 10,000-step recommendation for daily exercise was considered too difficult to achieve.”

Here’s new information that should take some of the pressure off: walking about half as many steps still has substantial health benefits.

I. Min Lee at Brigham and Women’s Hospital in Boston tracked 17,000 older women – average age 72 – to determine whether walking regularly would increase their life spans. It turns out that the women’s death rate declined by 40 percent when they walked just 4,400 steps a day.

Walking more than 4,400 steps is even better – but only up to a point. For every 1,000 additional steps beyond 4,400, the mortality rate declined, but the benefits stopped at around 7,500 steps per day, said the study, published in the May issue of the Journal of the American Medical Association.

More good news in the study for retirees is that it’s not necessary to walk vigorously to enjoy the health benefits. …Learn More

August 8, 2019

For Family, Caregiving is a Choice

Francey Jesson’s life took a dramatic turn in 2014 when she lost her job at Santa Fe, New Mexico’s airport after a dispute with the city. In 2015, she relocated to Sarasota, Florida to be close to her family. One day, her mother, who has dementia, started crying over the telephone.

Jesson had always known she would be her mother’s caregiver, and that time had arrived. She and her brother combined resources and bought a house in Sarasota, and Jesson and her mother moved in.

“It wasn’t difficult to decide. What was difficult was everything that came with it,” she said.

One reason for the rocky adjustment was that Jesson, who is single, had been preparing herself mentally to take care of her mother’s physical needs in old age. But Kay Jesson, at 88, is in pretty good health. She requires full-time care because she has cerebral vascular dementia, the roots of which can be traced back to a stroke more than 15 years ago.

She is still able to function and has not lost her social skills. Her muscle memory is also intact, allowing her to chop onions while her daughter cooks dinner. But she forgets to turn off the water in the bathtub, mixes up her pills, can’t remember who her great-grandchildren are, and is unable to distinguish fresh food from rotting food in the refrigerator.

She’s also developed a childlike impatience and constantly interrupts her daughter, who works from home for her brother’s online company. “When she’s hungry, she’s hungry,” Francey Jesson said about her mother.

“Nothing ever stops for me. I can’t sit in a room and not be interrupted,” she said. “Sometimes I just want to watch TV for an hour.”

One way she copes is to approach caregiving with a combination of love and bemusement. She uses “therapeutic fibbing” to protect her mother’s feelings, for example, telling her that a friend who died has moved instead to Kansas so she doesn’t grieve over and over again. Francey Jesson also resorts to humor in a blog she writes about her day-to-day experiences. In one article, “Debating with Dementia,” she recounted a conversation about the best way to repair some bathroom floor tile: …Learn More

August 1, 2019

A Proposal to Fill Your Retirement Gap

David and Debra S. both had successful careers. In analyzing their retirement finances, the couple agreed that he should wait until age 70 to start his Social Security in order to get the largest monthly benefit.

But he wanted to sell his business at age 69 and retire then, so the North Carolina couple used their savings to cover some expenses over the next year.

Waiting until 70 – the latest claiming age under Social Security’s rules – accomplished two things. In addition to ensuring David gets the maximum benefit, waiting guaranteed that Debra, who retired a few years ago, at 62, would receive the maximum survivor benefit if David were to die first.

Other baby boomers might want to consider using this strategy. As this blog frequently reminds readers, each additional year that someone waits to sign up for Social Security adds an average 7 percent to 8 percent to their annual benefit – and these yearly increments spill over into the survivor benefit.

Delaying Social Security is “the best deal in town,” said Steve Sass at the Center for Retirement Research, in a report that proposes baby boomers use the strategy to improve their retirement finances.

Here’s the rationale. Say, an individual wants a larger benefit. Instead of collecting $12,000 a year at age 65, he can wait until 66, which would increase his Social Security income to $12,860 a year, adjusted for inflation, with the increase passed along to his wife after his death (if his benefit is larger than his working wife’s own benefit). The cost of that additional Social Security income is the $12,000 the couple would have to withdraw from savings to pay their expenses while they delayed for that one year.

Social Security is essentially an annuity with inflation protection – and the payments last as long as a retiree does. So the $12,000 cost of increasing his Social Security benefit can be compared with cost of purchasing an equivalent, inflation-indexed annuity in the private insurance market. An equivalent insurance company annuity for a 65-year-old man, which begins paying immediately and includes a survivor benefit, would cost about $13,500. …Learn More

July 23, 2019

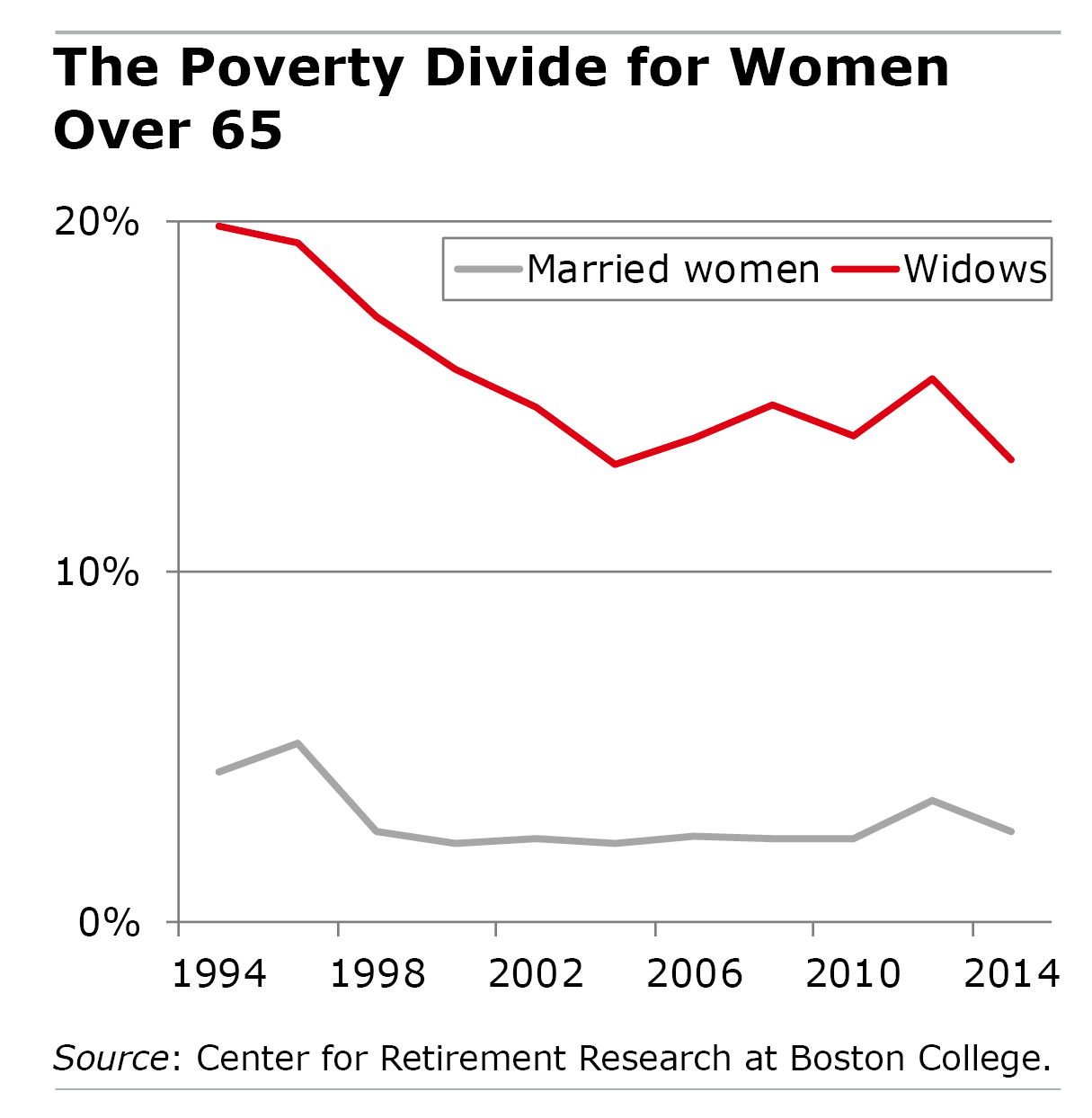

Expect Widows’ Poverty to Keep Falling

The poverty rate for widows has gone down over the past 20 years. This trend will probably continue for the foreseeable future.

The poverty rate for widows has gone down over the past 20 years. This trend will probably continue for the foreseeable future.

Women face the risk of slipping into poverty when a husband’s death triggers a drop in retirement income from Social Security and a pension (if he had one). But beginning in the 1970s and 1980s, women moved into the nation’s workplaces at an unprecedented pace.

Women now make up nearly half of the labor force and are more educated, which means better jobs – and better odds of having their own employer retirement plan. As a result, they have become increasingly financially independent.

This trend of greater independence is now showing up among older women. Widows between ages 65 and 85 put in 10 more years of work than their mother’s generation, which has helped push down the poverty rate from 20 percent in 1994 to 13 percent in 2014, according to the Center for Retirement Research. …Learn More

July 16, 2019

Spotlight on Our Research, Aug. 1-2

Topics for this year’s Retirement and Disability Research Consortium meeting include the opioid crisis, retirement wealth inequality over several decades, trends in Social Security’s disability program, and the impacts of payday loans, college debt, and mortgages on household finances.

Researchers from around the country will present their findings at the annual meeting in Washington, D.C. Anyone with an interest in retirement and disability policy is welcome. Registration will be open through Monday, July 29. For those unable to attend, the event will be live-streamed. The agenda lists all of the studies.

Here are a few:

- Why are 401(k)/IRA Balances Substantially Below Potential?

- The Impacts of Payday Loan Use on the Financial Well-being of OASDI and SSI Beneficiaries

- The Causes and Consequences of State Variation in Healthcare Spending for Individuals with Disabilities

- Forecasting Survival by Socioeconomic Status and Implications for Social Security Benefits

- What is the Extent of Opioid Use among Disability Applicants? …

July 11, 2019

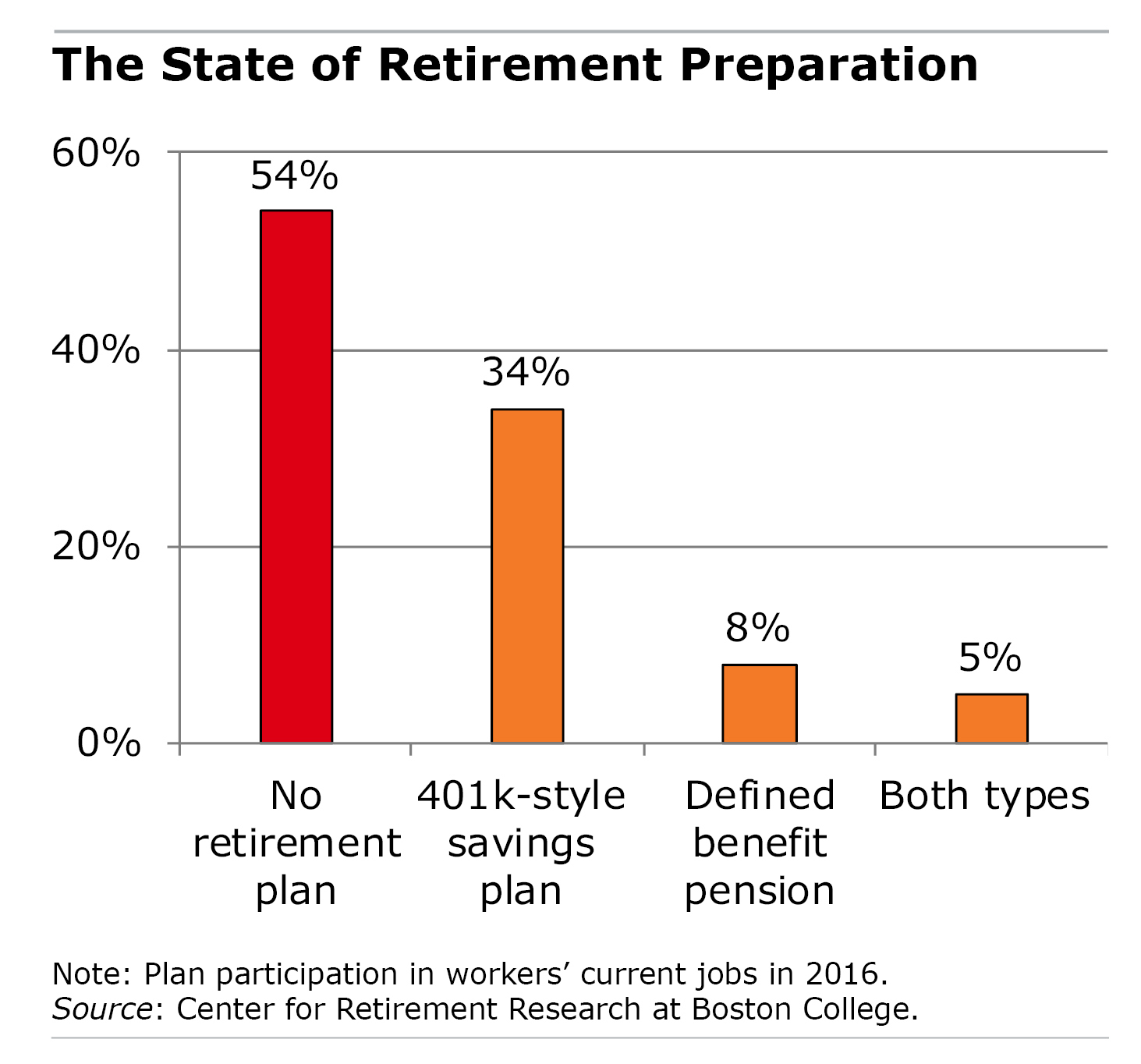

Video: Retirement Prep 101

Half of the workers who have an employer retirement plan haven’t saved enough to ensure they can retire comfortably.

This 17-minute video might be just the ticket for them.

Kevin Bracker, a finance professor at Pittsburg State University in Kansas, presents a solid retirement strategy to workers with limited resources who need to get smart about saving and investing.

While not exactly a lively speaker, Bracker explains the most important concepts clearly – why starting to save early is important, why index funds are often better than actively managed investments, the difference between Roth and traditional IRAs, etc.

Some of his figures are somewhat different than the data generated by the Center for Retirement Research, which sponsors this blog. But both agree on this: the retirement outlook is worrisome.

Some of his figures are somewhat different than the data generated by the Center for Retirement Research, which sponsors this blog. But both agree on this: the retirement outlook is worrisome.

The Center estimates that the typical baby boomer household who has an employer 401(k) and is approaching retirement age has only $135,000 in its 401(k)s and IRAs combined. That translates to about $600 a month in retirement.

Future generations who follow Bracker’s basic rules should be better off when they get old. …Learn More

July 9, 2019

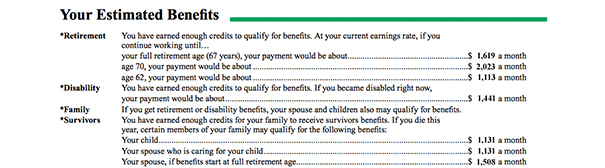

Social Security Statement Has Impact

When a Social Security statement comes in the mail, most people do not, as one might suspect, throw it on the pile of envelopes. They actually open it up and read it.

But are they absorbing the statements’ detailed estimates of how much money they’ll get from Social Security? RAND researcher Philip Armour tested this and found that the statement does, in fact, prompt people to stop and think about retirement: workers said their behavior and perceptions of the program changed after seeing the statement of their benefits.

The study was made possible after Social Security introduced a new system for mailing out statements. Workers used to get them in the mail every year. In 2011, the government took a hiatus and stopped sending them out. The mailings resumed in 2014 – but now they go out only before every fifth birthday (ages 25, 30, 35 etc.).

Armour was able to use the infrequent mailings to compare the reactions of the workers who had received a statement with those who had not during a four-year period, 2013-2017.

The statements bolstered their confidence that they could count on Social Security when they retire. More important, receiving them in the mail spurred some people to work more. To be clear, this is what they said – it isn’t known what they actually did.

Those who had been out of the labor market were much more likely, after getting a statement, to say they had returned to work. Working people under age 50 increased their hours of work.

Social Security benefits, on their own, usually are not enough to live on in retirement, and half of U.S. working-age households are at risk of falling short in retirement. But unfortunately, the study wasn’t able to detect another critical aspect of their retirement preparation: saving. …Learn More

About Squared Away

Learn more about our blog and its writer, Kimberly Blanton, a former Boston Globe reporter.